section 69 of CGST Act

section 69 of CGST Act provide for the power to arrest in GST.

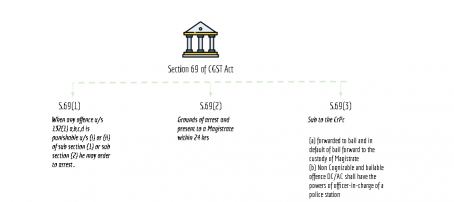

“(1) Where the Commissioner has reasons to believe that a person has committed any offence specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) of section 132 which is punishable under clause (i) or (ii) of sub-section (1), or sub-section (2) of the said section, he may, by order, authorise any officer of central tax to arrest such person.

(2) Where a person is arrested under sub-section (1) for an offence specified under subsection (5) of section 132, the officer authorised to arrest the person shall inform such person of the grounds of arrest and produce him before a Magistrate within twenty four hours.

Related Topic:

Arrest Under GST And Code Criminal Procedure, 1973 For Bail

(3) Subject to the provisions of the Code of Criminal Procedure, 1973,––

(a) where a person is arrested under sub-section (1) for any offence specified under sub-section (4) of section 132, he shall be admitted to bail or in default of bail, forwarded to the custody of the Magistrate;

(b) in the case of a non-cognizable and bailable offence, the Deputy Commissioner or the Assistant Commissioner shall, for the purpose of releasing an arrested person on bail or otherwise, have the same powers and be subject to the same provisions as an officer-in-charge of a police station.”

(As given in CGST Act)