ACCOMMODATION, FOOD AND BEVERAGE SERVICES

ACCOMMODATION, FOOD AND BEVERAGE SERVICES

GST has been a new buzz in the market since its rollout on July 01, 2017. Though over two years have been passed since its levy, still, people and industries are ambiguous of its impact on their businesses.

This article is an attempt to throw some light on one of the important sectors of the economy i.e. Hotel and Restaurants.

In the pre-GST regime era, a restaurant food bill attracted both VAT and Service Tax with VAT being levied on food component and Service Tax on the service component. GST has simplified the tax regime by submerging many indirect taxes into one.

Many changes have been made via various notifications for hotel and restaurant services which have been captured below in sequence of their release.

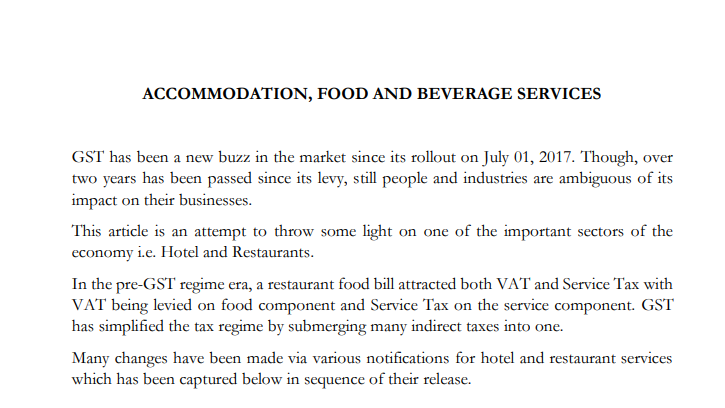

Entry No. 7 of Notification 11/2017 of Central Tax (Rate) deals with Accommodation, food and beverage services.

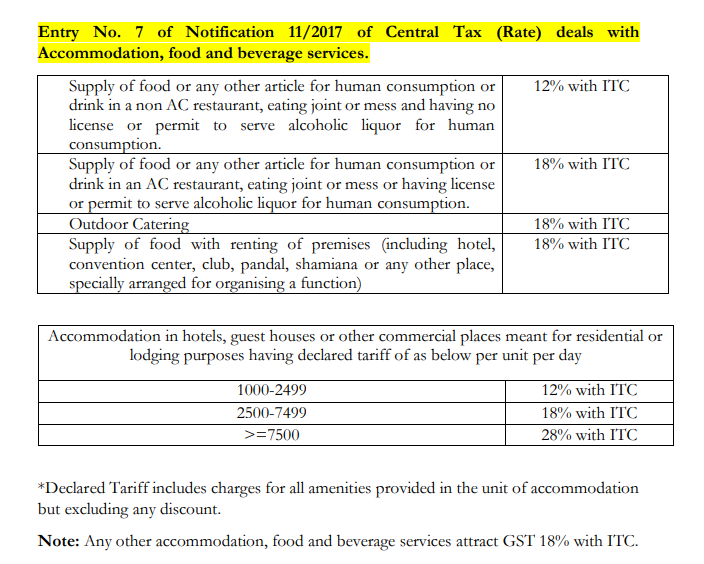

Changes via Notification 46/2017 Central Tax (Rate) w.e.f 15.11.2017

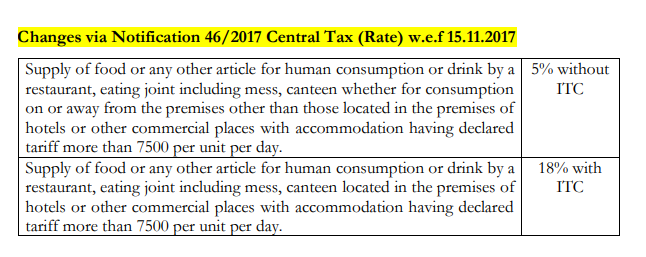

Changes via Notification 13/2018 Central Tax (Rate) w.e.f 27.07.2018

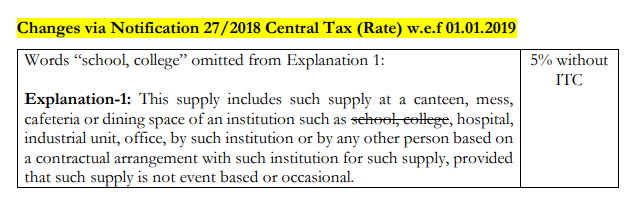

Changes via Notification 27/2018 Central Tax (Rate) w.e.f 01.01.2019

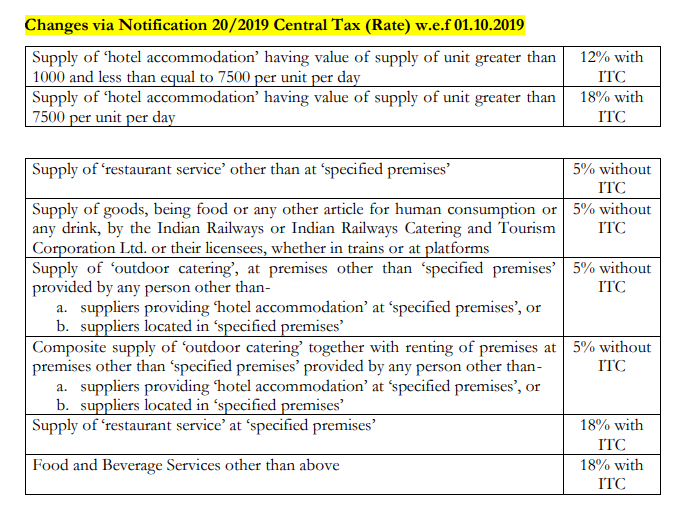

Changes via Notification 20/2019 Central Tax (Rate) w.e.f 01.10.2019

*‘Specified premises’ means premises providing ‘hotel accommodation’ services having declared tariff of any unit of accommodation above seven thousand five hundred rupees per unit per day.

Download the copy: