Clinical research is not Export: Cliantha AR

Introduction:

Clinical research is a buzzing service in India. The supplier provides the services of clinical research for the recipient located outside India. In these services, various activities related to research are done. Now whether that service will be an export of service or not. The litmus test for this will be its place of supply. It is in India than it is not an export. Place of supply should fall in India to make it export of service. In this advance ruling of Maharastra AAR , this issue is discussed. Cliantha research limited advance ruling of Maharashtra is relevant to this isuues.

What is clinical research service?

“clinical research” means doing the research on the medicinal products or drugs invented by a person. In these services drug is provided by the recipient of service. The supplier will do research of that drug on various human. A report based on its reactions will be made and provided to the recipient.

What will be the place of supply in case of clinical research?

Now the question for GST is, what is Pos in this case. The provisions of the place of supply of section 13 of the CGST Act provide for this situation. There are two possible parts of the section where it can be covered:

- Section 13(2): PoS will be the location of the recipient.

- Section 13(3): Pos will be the location of goods when services were executed.

The first case is applicable when the case is not falling in any from 3 to 13.

If it is falling in 13(3), which is more specific it will not fall in 13(1). Section 13(3) covers the situation where the services are provided on some goods. The location of goods at the time of execution will be the place of supply.

Whether clinical research done for a foreign company will be an Export or not?

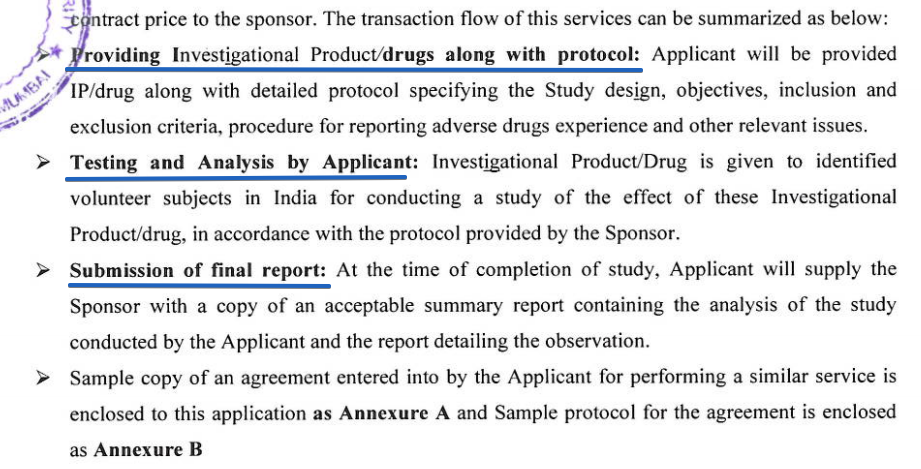

Guidance from the advance ruling of Cliantha research limited. In this ruling, this aspect is discussed in detail. The company is engaged in clinical research. Thye needs to do the following activities for their research.

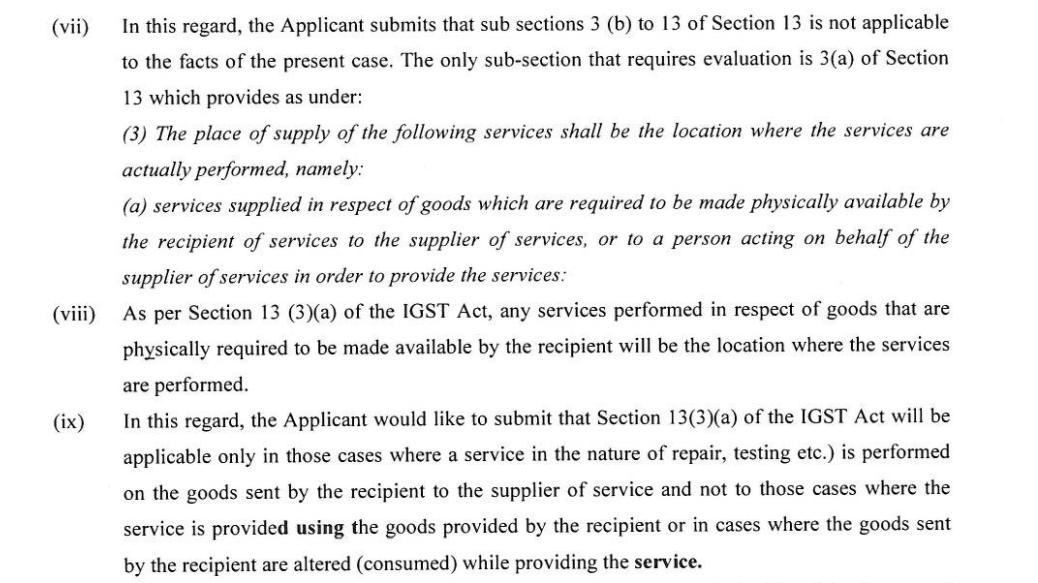

The medicine was provided by the recipient of services. The applicant said that this will not be covered in section 13(1) because in this case goods were consumed during services. Section 13(3) covers only the case where some activity on goods is required like, repair. Following facts were added to rebut the applicability of 13(3).

Clinical research is not export in GST: Cliantha research AR(Maha)

It was held by the authority that there is no such requirement that activity should be on goods. The provisions of section 13(3) will apply even if goods are consumed during the process of services.

Hence clinical research is not export. The PoS is in India because section 13(1) will be applicable.

CA