Section 66 of CGST Act: Special audit in GST(Updated till July 2024)

Section 66 of CGST Act

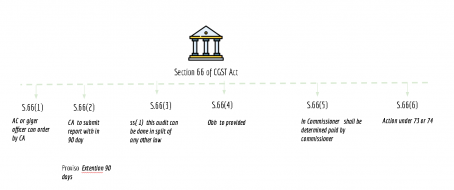

Section 66 of CGST Act provide for the special audit in GST.

“(1) If at any stage of scrutiny, inquiry, investigation or any other proceedings before him, any officer not below the rank of Assistant Commissioner, having regard to the nature and complexity of the case and the interest of revenue, is of the opinion that the value has not been correctly declared or the credit availed is not within the normal limits, he may, with the prior approval of the Commissioner, direct such registered person by a communication in writing to get his records including books of account examined and audited by a chartered accountant or a cost accountant as may be nominated by the Commissioner.

(2) The chartered accountant or cost accountant so nominated shall, within the period of ninety days, submit a report of such audit duly signed and certified by him to the said Assistant Commissioner mentioning therein such other particulars as may be specified:

Provided that the Assistant Commissioner may, on an application made to him in this behalf by the registered person or the chartered accountant or cost accountant or for any material and sufficient reason, extend the said period by a further period of ninety days.

(3) The provisions of sub-section (1) shall have effect notwithstanding that the accounts of the registered person have been audited under any other provisions of this Act or any other law for the time being in force.

(4) The registered person shall be given an opportunity of being heard in respect of any material gathered on the basis of special audit under sub-section (1) which is proposed to be used in any proceedings against him under this Act or the rules made thereunder.

(5) The expenses of the examination and audit of records under sub-section (1), including the remuneration of such chartered accountant or cost accountant, shall be determined and paid by the Commissioner and such determination shall be final.

(6) Where the special audit conducted under sub-section (1) results in detection of tax not paid or short paid or erroneously refunded, or input tax credit wrongly availed or utilised, the proper officer may initiate action under section 73 or section 74.”

(As given in CGST Act)

Consultant