Original copy of order OF GST AAR of E-DP Marketing Private Limited

Introduction:

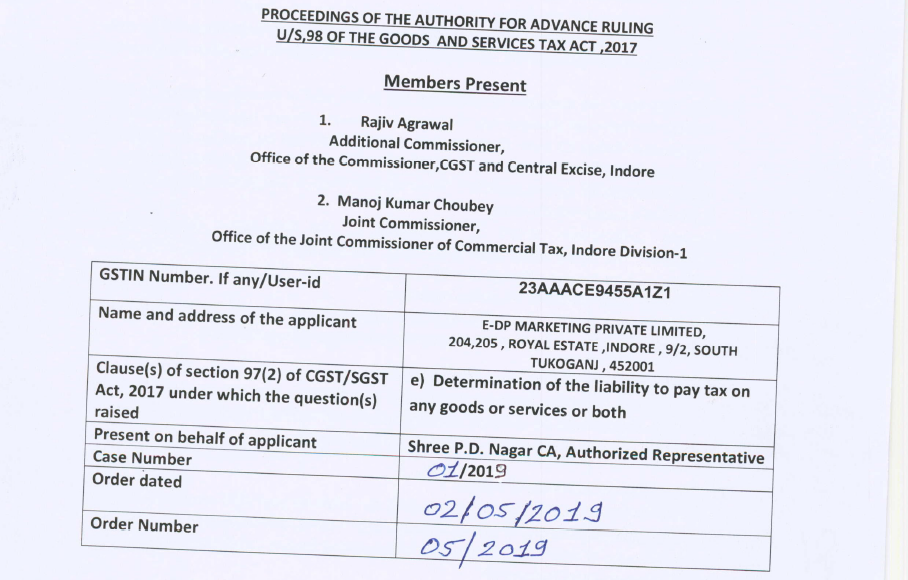

This is an original copy of advance ruling of E-DP marketing private limited.

PROCEEDINGS

(Under sub-section (4) of Section 98 of Central Goods and Service Tax Act, 2017 and the Madhya Pradesh Goods & Service Tax Act, 2017)

1. The present application has been filed u/s 97 of the Central Goods & Services Tax Act, 2017 and MP Goods & Services Tax Act, 2017 (hereinafter also referred to CGST Act and MPSGT Act respectively) by M/s. E-DP MARKETING PRIVATE LIMITED (hereinafter referred to as the Applicant), registered under the Goods & Services Tax.

2. The provisions of the CGST Act and MPGST Act are identical, except for certain provisions. Therefore, unless a specific mention of the dissimilar provision is made, a reference to the CGST Act would also mean a reference to the same provision under the MPGST Act. Further, henceforth, for the purposes of this Advance Ruling, a reference to such a similar provision under the CGST or MP GST Act would be mentioned as being under the GST Act.

3. BRIEF FACTS OF THE CASE:

3.1 That the applicants holding GSTN No. 23AAACE9455A1Z1 is engaged in the trading of various edible oils are falling under Chapter 15 of the GST Tariff.

3.2 That the applicant intend to import crude soyabean oil on CIF basis (Cost + Insurance + Freight) which includes the component of ocean freight in the price of imported goods.

3.3 The applicants are required to authorize the seller who is a person located in non- taxable territory for transporting the goods by a vessel from the supplier’s place up to the place in Indian Custom Territory. Ocean Freight will not be paid by the applicant because the seller is supposed to collect the ocean freight while deciding the price of the Goods payable by the applicant. The payment of ocean freight would be made by the seller located outside India.

3.4 As per corrigendum issued on 30.06.2017 to the Notification No. 8/2017— Integrated Tax (Rate) dated 28th June 2017, the importer of the goods is required to pay IGST on Reverse Charge Mechanism on the amount of deemed ocean freight equal to 10% of the value of goods imported.

35 The issue raised by the applicant is on Applicability of Reverse Charge Mechanism on Ocean Freight when IGST is paid by the importer on Goods Imported on CIF Basis.

4. QUESTIONS RAISED BEFORE THE AUTHORITY:-

Whether the applicant /importer is again required to pay IGST on the component of ocean freight under RCM mechanism on the deemed amount which will amount to double taxation of IGST on the deemed component of ocean freight of the imported goods?

5. CONCERNED OFFICERS’ VIEWPOINT:

The Concerned Officer Submitted that Applicant shall be liable to pay IGST on ocean freight paid on imported goods under Reverse Charge Mechanism in terms of Notification No.10/2017- YY IT(R) and Notification No.8/2017-IT(R) irrespective of the ocean freight component having been a part of the CIF value of imported goods.

6 RECORD OF PERSONAL HEARING: Shree P.D. Nagar CA, Authorized Representative of the applicant appeared for personal hearing and reiterated the submissions already made in the application. The Applicant states that-

6.1 That the applicants are engaged in the manufacture of various edible oils which are falling under Chapter 15 of the GST Tariff and for the same they are holding GSTN No.23AAACR2892L7Z0.

6.2 That the applicant intend to import crude soya bean oil on CNF (Cost plus Freight) or CIF (Cost + Insurance + Freight) basis which includes the component of ocean freight into the price of imported goods.

6.3 Under these circumstances the applicants are required to authorize the seller who is a person located in non-taxable territory for transporting the above goods by a vessel from supplier’s place up to the place in Indian Custom station. The seller collects the ocean freight in the price of goods from the buyer i.e. applicant.

6.4 It is submitted that at the time of import of said goods into India the applicant is required to pay aggregate customs duties on CNF/CIF value of the imported goods which is considered as an assessable value for the purpose of levying the import duties on such goods and which includes IGST component also. Since the CNF/CIF value of the imported goods includes the component of ocean freight therefore, the applicant is required to pay IGST on this ocean freight component also along with other duties of customs. This is the first incidence of payment of IGST on the component of ocean freight by the applicant. We are enclosing herewith 2/3 specimen copies of relevant Bills of Entry of imported goods showing payment of IGST on ocean freight element of the imported goods.

6.5 Further, it was argued that the Notification No. 10/2017—Integrated Tax (Rate) dated 28th June 2017, in which as per item No. 10, the applicant is again required to pay IGST on ocean freight incurred by them in respect of imported cargo under the RCM mechanism. Relevant entry No. 10 reads as under -SI. No. Category of supply of Services Supplier of Service Recipient of Service10Services supplied by a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India A person located in non-taxable territory Importer, as defined in clause (26) of section 2 of the Customs Act, 1962 (52 of 1962), located in the taxable territory.

6.6. The Applicant stated that as per aforesaid Notification, the applicant /importer is again required to pay IGST on the component of ocean freight incurred by them under RCM mechanism. If this is paid by the applicant/importer, it will amount to double taxation of IGST on the same component of ocean freight of the imported goods which apparently illegal and against the basic principles GST of law. Copy of aforesaid Notification No. 10/2017- Integrated Tax (Rate) dated 28th June 2017 is attached herewith for your ready reference.

6.7. From the facts mentioned above, it is clear that the Department will be charging IGST on vessel ocean freight twice which amounts to double taxation.

6.8 It is settled law that there should not be any double taxation of the same tax on the same goods.

7. DISCUSSIONS AND FINDINGS:

7.1 We have carefully considered the submissions made by the applicant in the application, the pleadings on behalf of the Applicant made during the course of personal hearing. At the outset, we find that the issue raised in the Application is squarely covered under Section 97(2)(e) of the CGST Act 2017 is a matter related to determination of the liability to pay tax on any goods or services or both, and the applicant has complied with the all the requirements for filing this application as laid down under the law. We, therefore, admit the application for consideration on merits.

7.2 The Applicant, vide instant application, has posted the following question before us, seeking ruling on the same — Whether the Applicant/importer is again required to pay IGST on the component of ocean freight under RCM (Reverse Charge Mechanism) on deemed amount which will amount to double taxation of IGST on deemed component of ocean freight of the imported goods?

7.3 As detailed in foregoing paras, the Applicant is engaged in trading of various edible oils. It has been mentioned in the application that the applicant intends to import crude Soyabean Oil on CIF (Cost+Insurance+Freight) basis, which includes the component of ocean freight in the price of imported goods. Obviously, in case of such imports, the seller is located in non-taxable territory, the ocean freight is collected by the seller from the importer located in the taxable territory. However, as per Notification 10/2017-Integrated Tax (Rate) dtd.28.06.2017, [Sr.No.10], the ‘Services supplied by a person located in non-taxable territory by way of transportation of goods be a vessel from a place outside India up to the customs station of clearance in India’ have been put under Reverse Charge Mechanism and the recipient of service viz. ‘Importer, as defined in clause (26) of Section 2 of the Customs Act 1962 (52 of 1962), located into the taxable territory’.

7.4 Further, in terms of Notification No.8/2017-Integrated Tax (Rate) dtd.28.06.2017, read with Corrigendum dtd.30.06.2017, the taxable value in respect of ocean freight has been defined as, ‘Where the value of taxable service provided by a person located in non-taxable territory to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India is not available with the person liable for paying integrated tax, the same shall be deemed to 10% of the CIF value (sum of cost, insurance and freight) of imported goods’

7.51n view of the above two notifications we do not find any ambiguity, whatsoever, regarding payment of IGST on ocean freight. As per existing law, IGST on ocean freight has to be paid by the importer under reverse charge mechanism, irrespective of the fact that such freight charges are included in the intrinsic CIF value.

7.6 We find from the application that the applicant has pleaded that the authority to levy and collect IGST on import of goods from outside India vests under the Customs Act only hence on deemed value of ocean freight the levy of RCM is without jurisdiction. As we could construe, the applicant has broadly challenged the validity of levy of IGST on ocean freight under RCM. We observe that any question relating to constitutional validity of the Notifications issued is not within the ambit of the jurisdiction of this Authority. Nevertheless, it is pertinent to mention here that the Notifications are issued on the basis of the recommendations of the GST Council, and the GST Council in turn is empowered by the provisions of Article 279A(4) of the Constitution of India inserted vide the Constitution (One Hundred and First Amendment0 Act, 2016, to make recommendation to the Union and States on-

a. The taxes, cesses and surcharges levied by the Union, the States and the local bodies, which may be subsumed in the goods and services tax;

c. model goods and services tax laws, principles of levy, apportionment of goods and services tax levied on supplies in the course of interstate trade or commerce under Article 269A and the principles that govern the place of supply;

h. any other matter relating to the Goods and Services tax as the Council may decide

7.7 It is thus clear that any notification is issued only as per recommendations of the GST Council, and the law laid down is binding upon the concerned. We find that the applicant has questioned the levy under RCM as being without jurisdiction. As already spelled out, this Authority does not have the jurisdiction or authority to dwell into this question, in terms of Section 97(2) of the Act ibid. However, we reiterate that in terms of prevailing provisions of the IGST Act 2017 and the Rules made thereunder, the applicant is liable to pay IGST on ocean freight under RCM as provided under Notification No.10/2017-IT (R) read with Notification No.8/2017-IT(R).

8.RULING

(Under section 98 of Central Goods and Services Tax Act, 2017 and the Madhya Pradesh Goods and Services Tax Act, 2017)

8.1 The Applicant shall be liable to pay IGST on ocean freight paid on imported goods under Reverse Charge Mechanism in terms of Notification No.10/2017-IT(R) and Notification No.8/2017-IT(R) irrespective of the ocean freight component having been a part of the CIF value of imported goods.

8.2 This ruling is valid subject to the provisions under section 103(2) until and unless declared void under Section 104(1) of the GST Act.

Consultant