Advisory for filing refund application under GST-RFD-01A

Advisory to taxpayers for filing refund application under GST-RFD-01A

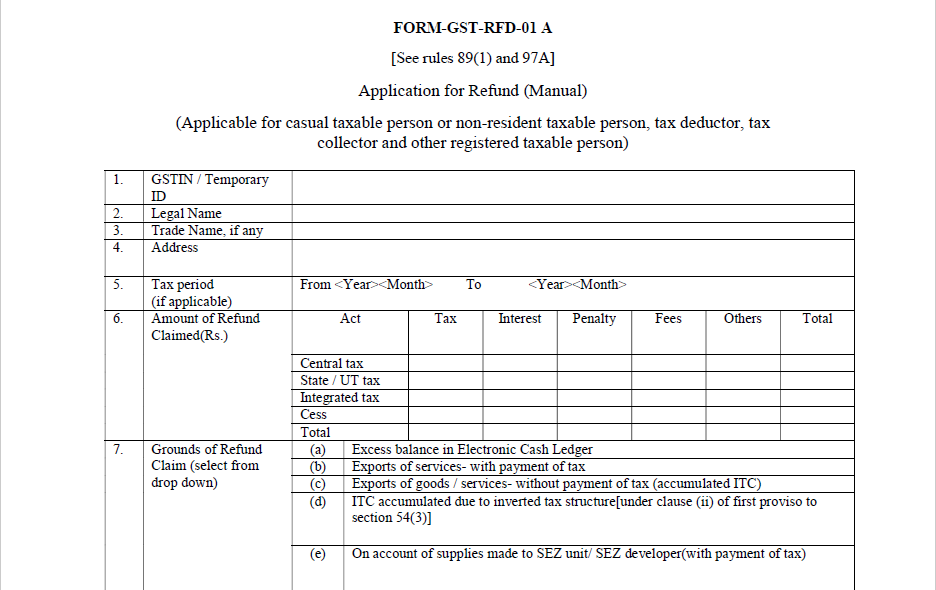

Advisory to taxpayers for filing refund application under GST-RFD-01A:

1. Refund application can be filed using the application form GST-RFD-01A.

2. Refund application filing for multiple tax period is available for the below ground of refunds:

– Export of Goods and Services – Without payment of Tax

– Supplies made to SEZ Unit/SEZ Developer – Without payment of Tax

3. The taxpayer would have to provide the tax period details for which refund has to be claimed.

4. The multiple tax period application has following restrictions:

a. Multiple tax period selection should be within a financial year

b. The application has to be filed chronologically for tax periods and in case refund application is not to be filed for any tax period, a declaration of ‘No Refund Application is to be provided’.

For e.g.: April 2018 to June 2018 refund application cannot be filed till application or No refund application declaration is filed for any tax period prior to April 2018

5. For claiming the refund, the taxpayer would have to upload the invoice details in the statement template available in the refund application itself.

6. Statement upload is mandatory. The taxpayer shall provide all the required details in the statement template. The statement uploaded by the taxpayers shall be validated by the system from the invoice data declared/provided by the taxpayer at the time of filing the return for that period for which refund is to be claimed.

7. Only after validating the data from the system, the taxpayer would be able to fie the application.

8. All the invoice details are to be provided in a single statement. The taxpayer need not upload multiple statements for different periods separately.

9. Once the taxpayer has provided the details of the invoice for a particular period and the same is checked and validated from GSTR-1 returns data by the system on upload.

10. Once, an invoice is included in the application’s statement, the same will be marked as non-amendable and non-refundable for future.

11. After filing the application, the taxpayer would not be able to claim the refund for that invoice again in some other refund application as the system will lock the invoice for which refund is claimed in one application. Also, the taxpayer would not be able to amend the invoice details after claiming the refund.

12. The taxpayer can also attach any other supporting documentation is required to be attached with the application. 4 documents can be uploaded with a single application in pdf format. Maximum size allowed for a document is 5MB.

13. After filing of refund application by the taxpayer, refund application form GST-RFD-01A along with the statement and documents uploaded shall be available to tax officer for review and processing of refund application.

14. The taxpayer can track the status of the application on the portal using “Track Application Status” functionality.

15. As the functionality for multiple tax period has been made available, therefore to avoid duplication, the refund applications in the categories mentioned in point 2 above that were SAVED in the GST system will be purged and removed from the system.

CA Amresh Vashisht

For Updates 9837515432