Expert Knowledge,

Straight from Practitioners.

Tax tips, legal guides, and financial advice written by the same verified CAs, Advocates, and Advisors you can consult on ConsultEase.

CGST Rule 96A: Refund of tax paid on export under bond or LUT

CGST Rule 96A: Refund of integrated tax paid on export of goods or services under bond or LUT (Letter of Undertaking) (1) Any registered person availing the option to supply goods or services for export without payment of integrated tax shall furnish, prior to export,

CA Shafaly Girdharwal

CA Shafaly GirdharwalCGST Rule 96: Refund of integrated tax paid on goods exported

CGST Rule 96: Refund of integrated tax paid on goods exported out of India. (1) The shipping bill filed by an exporter shall be deemed to be an application for refund of integrated tax paid on the goods exported out of India and such application

CA Shafaly Girdharwal GST Compliance

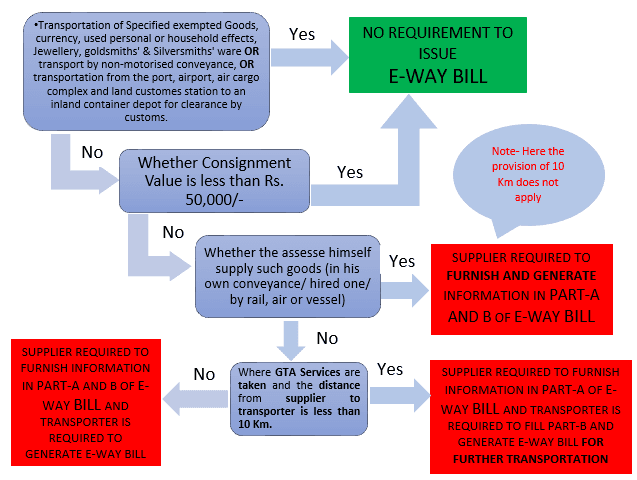

GST ComplianceE-Way bill — Flowchart & amp and salient features

Salient Features of E-way Bill: – 1. Before commencement (where consignment value is greater than Rs. 50,000/-) – Furnish information Electronically in Part-A of Form GST EWB-01. This information is required even if the transportation distance is less than 10 Km. This information will be made available to the recipient, who shall communicate his acceptance or rejection. 2. When Goods

CA Ashutosh Sharma

CA Ashutosh SharmaCGST Rule 138 D : Facility for uploading information regarding detention of vehicle

CGST Rule 138 D : Facility for uploading information regarding detention of vehicle Where a vehicle has been intercepted and detained for a period exceeding thirty minutes, the transporter may upload the said information in FORM GST EWB-04 on the common portal. FORM GST EWB-01 (See rule

CA Shafaly GirdharwalCGST Rule 138 C : Inspection and verification of goods

CGST Rule 138 C : Inspection and verification of goods (1) A summary report of every inspection of goods in transit shall be recorded online by the proper officer in Part A of FORM GST EWB-03 within twenty four hours of inspection and the final report

CA Shafaly GirdharwalCGST Rule138 B : Verification of documents and conveyances

CGST Rule 138 B : Verification of documents and conveyances (1) The Commissioner or an officer empowered by him in this behalf may authorise the proper officer to intercept any conveyance to verify the e-way bill or the e-way bill number in physical form for

CA Shafaly GirdharwalCGST Rule 138 A : Documents and devices to be carried by a person-in-charge of a conveyance

CGST Rule 138 A : Documents and devices to be carried by a person-in-charge of a conveyance (1) The person in charge of a conveyance shall carry— (a) the invoice or bill of supply or delivery challan, as the case may be; and (b) a

CA Shafaly GirdharwalCGST Rule 138 : E-way bill rules in GST

CGST Rule 138 : E-way bill rules Till such time as an E-way bill system is developed and approved by the Council, the Government may, by notification, specify the documents that the person in charge of a conveyance carrying any consignment of goods shall carry

CA Shafaly GirdharwalCGST Rule 137 : Tenure of Authority

CGST Rule 137 : Tenure of Authority The Authority shall cease to exist after the expiry of two years from the date on which the Chairman enters upon his office unless the Council recommends otherwise. Explanation.-For the purposes of this Chapter, (a) “Authority” means the National Anti-profiteering

CA Shafaly GirdharwalCGST Rule : 136 Monitoring of the order

CGST Rule : 136 Monitoring of the order The Authority may require any authority of central tax, State tax or Union territory tax to monitor the implementation of the order passed by it. (Updated upto September 2017)

CA Shafaly GirdharwalCGST Rule 135: Compliance by the registered person

CGST Rule 135: Compliance by the registered person Any order passed by the Authority under these rules shall be immediately complied with by the registered person failing which action shall be initiated to recover the amount in accordance with the provisions of the Integrated Goods and

CA Shafaly GirdharwalCGST Rule 134: Decision to be taken by the majority

CGST Rule 134: Decision to be taken by the majority If the Members of the Authority differ in opinion on any point, the point shall be decided according to the opinion of the majority. (Updated upto September 2017)

CA Shafaly Girdharwal