Expert Knowledge,

Straight from Practitioners.

Tax tips, legal guides, and financial advice written by the same verified CAs, Advocates, and Advisors you can consult on ConsultEase.

GST Compliance

GST ComplianceThe Constitutional Validity of Section 13(8)(B) of IGST Act 2017

Various pre-GST concepts were transitioned into the GST era, but many were embedded with legacy disputes as well. To mention the best illustration, ‘Intermediary ’ could be one of them. Hon’ble Gujarat High Court in case of Material Recycling Association of India vs Union

GST Compliance

GST ComplianceGuidance notes on How to fill Box No.12 of GSTR-1 as per recent amendments w.e.f. 01.04.2021 of GST Law,2017.

Dear Professional Colleagues, Good Day to you. I have gone through recent changes about mandatory to mention HSN & SAC Code in Tax Invoice and furnishing inward & outward details at box no 12 of GSTR-1 w.e.f.01.04.2021. Some of the professionals are having confusion

GST Compliance

GST ComplianceHigh Court’s protective shield against the mindless provisional attachment

In terms of S.83 of the CGST Act, 2017, the Commissioner has the powers to provisionally attach the property, including a bank account belonging to a taxable person under certain specified circumstances. When any proceedings under the specified provisions are pending against a taxable

GST Compliance

GST ComplianceKerala issues first guidelines on blocking/unblocking of Input Tax Credit

Circular bases on ‘Rule 86A’ of GST Rules; experts say CBIC should ensure its uniformity across the nation Kerala has come out with detailed circular and Standard Operating Procedures (SoP) to streamline the process of blocking/unblocking of Input Tax Credit (ITC). Kerala is the

Important FAQs About GST Amnesty Scheme 2021 for Waiver of Late Fees

Introduction of GST Amnesty Scheme 2021 Amnesty means providing relief from some penal action. Recently GST amnesty scheme 2021 is announced by CBIC. It is a scheme to waive late fees. The fees are accumulated due to non-filing or late filing of returns. FAQ’s on

CA Shafaly Girdharwal

CA Shafaly Girdharwal GST Compliance

GST ComplianceJoint Development Agreement (JDA): Landowner’s Share – ITC And Time of Supply

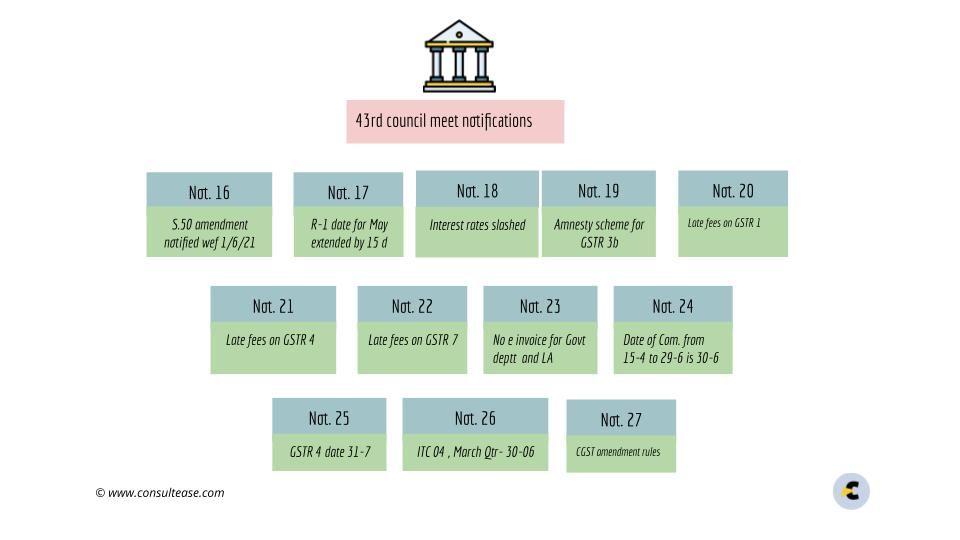

Amendment In 43rd GST Council Meeting And Notifications Dt. 02.06.2021 In an Area Sharing Joint Development Agreement: Landowner transfers development rights of their owned land to Developer and The developer develops and constructs superstructure inter-ala for the landowner on the Landowner’s share of Land. 2.

Important changes in GST returns, GSTR 3b and 1

Introduction- Due to lockdown, CBIC has amended the due date of GST returns. Also, the Input tax credit for 36(4) can also be adjusted cumulatively till June 2021. These changes are introduced via various notifications issued on 1st June 2021. It was recommended by the

CA Shafaly Girdharwal GST Compliance

GST ComplianceThe unsavoury controversy of IGST exemption to the import of oxygen concentrators

For the past almost two years, Covid-19 Pandemic has gripped the world and the Indian Sub-Continent cannot be expected to remain immune to this life-threatening virus. In fact, the ‘second wave’ of this Pandemic has turned out to be much more lethal than the

GST Compliance

GST ComplianceImportant changes in GST Return, Interest and Rules

Not. 16/2021 Provisions of Section 112 of FA 2021 is notified applicable from 1st July 2017 112. In section 50 of the Central Goods and Services Tax Act, in sub-section (1), for the proviso, the following proviso shall be substituted and shall be deemed

GST Compliance

GST ComplianceUpdated Due Dates Chart

Aggregate Turnover In The Preceding Fy More Than Rs. 5 Crore (> Rs 5 Cr) {NN 18/2021-CT & NN 19/2021-CT Dt. 01.06.21} Tax Period Actual Due Date Late Fee Interest Relaxation (Days) Last date to Avail Benefit Relaxation (Days) NIL 9% Reduced Rate 18%

GST Compliance

GST ComplianceTax Connect’s Analysis of Notifications To Give Effect To The Recommendations of 43rd GST Council Meeting Held On 28th May 2021

1. Relating To Real Estate – Notification No. 02/2021 – Central Tax (Rate) & Notification No. 03/2021 – Central Tax (Rate) In the 43rd Meeting of The GST Council, it was recommended to allow credit to landowners in joint development agreements even before the completion

GST Compliance

GST ComplianceNational Informatics Centre Release Notes: 01/06/2021

With reference Notification, 15/2021-CT dated 18.05.2021, to blocking of GSTIN for e-Way Bill generation is now considered only for the defaulting Supplier GSTIN and not for the defaulting Recipient or Transporter GSTIN. Click on the notification for more details. Mode of transport Ship is