Expert Knowledge,

Straight from Practitioners.

Tax tips, legal guides, and financial advice written by the same verified CAs, Advocates, and Advisors you can consult on ConsultEase.

CGST (Rates) all notifications

CGST (Rates) all notifications 30/2017-Central Tax (Rate) ,dt. 29-09-2017 Exempting supply of services associated with transit cargo to Nepal and Bhutan. 29/2017-Central Tax (Rate) ,dt. 22-09-2017 Seeks to amend notification no. 5/2017- central tax(rate) dated 28.06.2017 to give effect to gst council decisions regarding restriction

CA Shafaly Girdharwal

CA Shafaly GirdharwalCGST Rule 96A: Refund of tax paid on export under bond or LUT

CGST Rule 96A: Refund of integrated tax paid on export of goods or services under bond or LUT (Letter of Undertaking) (1) Any registered person availing the option to supply goods or services for export without payment of integrated tax shall furnish, prior to export,

CA Shafaly GirdharwalCGST Rule 138 C : Inspection and verification of goods

CGST Rule 138 C : Inspection and verification of goods (1) A summary report of every inspection of goods in transit shall be recorded online by the proper officer in Part A of FORM GST EWB-03 within twenty four hours of inspection and the final report

CA Shafaly Girdharwal GST Compliance

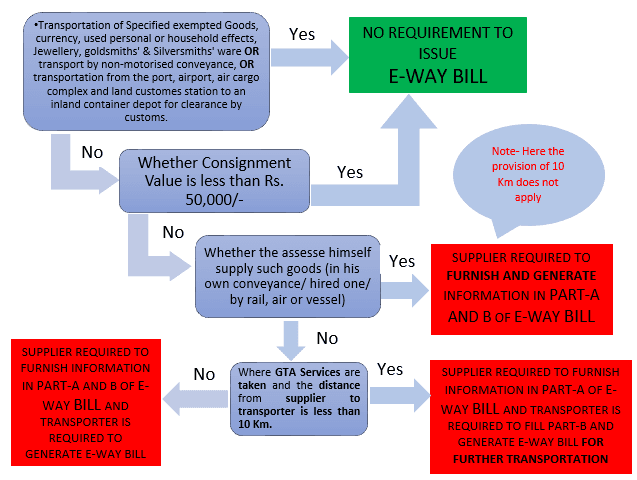

GST ComplianceE-Way bill — Flowchart & amp and salient features

Salient Features of E-way Bill: – 1. Before commencement (where consignment value is greater than Rs. 50,000/-) – Furnish information Electronically in Part-A of Form GST EWB-01. This information is required even if the transportation distance is less than 10 Km. This information will be made available to the recipient, who shall communicate his acceptance or rejection. 2. When Goods

CA Ashutosh Sharma

CA Ashutosh SharmaCGST Rule 138 A : Documents and devices to be carried by a person-in-charge of a conveyance

CGST Rule 138 A : Documents and devices to be carried by a person-in-charge of a conveyance (1) The person in charge of a conveyance shall carry— (a) the invoice or bill of supply or delivery challan, as the case may be; and (b) a

CA Shafaly GirdharwalCGST Rule138 B : Verification of documents and conveyances

CGST Rule 138 B : Verification of documents and conveyances (1) The Commissioner or an officer empowered by him in this behalf may authorise the proper officer to intercept any conveyance to verify the e-way bill or the e-way bill number in physical form for

CA Shafaly GirdharwalCGST Rule 138 D : Facility for uploading information regarding detention of vehicle

CGST Rule 138 D : Facility for uploading information regarding detention of vehicle Where a vehicle has been intercepted and detained for a period exceeding thirty minutes, the transporter may upload the said information in FORM GST EWB-04 on the common portal. FORM GST EWB-01 (See rule

CA Shafaly GirdharwalCGST Rule 96: Refund of integrated tax paid on goods exported

CGST Rule 96: Refund of integrated tax paid on goods exported out of India. (1) The shipping bill filed by an exporter shall be deemed to be an application for refund of integrated tax paid on the goods exported out of India and such application

CA Shafaly GirdharwalCGST Rule 138 : E-way bill rules in GST

CGST Rule 138 : E-way bill rules Till such time as an E-way bill system is developed and approved by the Council, the Government may, by notification, specify the documents that the person in charge of a conveyance carrying any consignment of goods shall carry

CA Shafaly GirdharwalCGST Rule 122: The Authority in GST

CGST Rule 122: The Authority shall consist of (a) a Chairman who holds or has held a post equivalent in rank to a Secretary to the Government of India; and (b) four Technical Members who are or have been Commissioners of State tax orcentral tax

CA Shafaly GirdharwalCGST Rule 123: Constitution of the Standing Committee and Screening Committees

CGST Rule 123: Constitution of the Standing Committee and Screening Committees (1) The Council may constitute a Standing Committee on Anti-profiteering which shall consist of such officers of the State Government and Central Government as may be nominated by it. (2) A State level Screening

CGST Rule 126: Power to determine the methodology and procedure

CGST Rule 126: Power to determine the methodology and procedure The CGST rule 126 describes about power to determine the methodology and procedure: The Authority may determine the methodology and procedure for determination as to whether the reduction in the rate of tax on the