Expert Knowledge,

Straight from Practitioners.

Tax tips, legal guides, and financial advice written by the same verified CAs, Advocates, and Advisors you can consult on ConsultEase.

Income Tax Compliance

Income Tax ComplianceSection 194Q vis a vis Section 206C(1H)

Section 194Q 206C (1H) Applicability w.e.f 01-July-2021 w.e.f 01-Oct-2020 Who (Deductor/Collector) Every Buyer whose turnover (Excluding GST) in Preceding F.Y. is More than Rs. 10 Crore (While Calculating this turnover value of goods and services both included) Every Seller whose turnover (Excluding GST) in

GST Compliance

GST ComplianceUpdated Due Dates Chart

Aggregate Turnover In The Preceding Fy More Than Rs. 5 Crore (> Rs 5 Cr) {NN 18/2021-CT & NN 19/2021-CT Dt. 01.06.21} Tax Period Actual Due Date Late Fee Interest Relaxation (Days) Last date to Avail Benefit Relaxation (Days) NIL 9% Reduced Rate 18%

Income Tax Compliance

Income Tax ComplianceTDS(tedious) and TCS Overall Analysis

Analysis of TDS provisions as per Income Tax Act (“the Act” or “IT Act”) Salary Related – 192 AND 192A Section Nature of payment Payer Payee Rate Remarks 192 Salary Any person Employee (R or NR) Slab rate Note 1 192A Accumulated balance of a

CA Sangam Kumar Aggarwal

CA Sangam Kumar Aggarwal GST Compliance

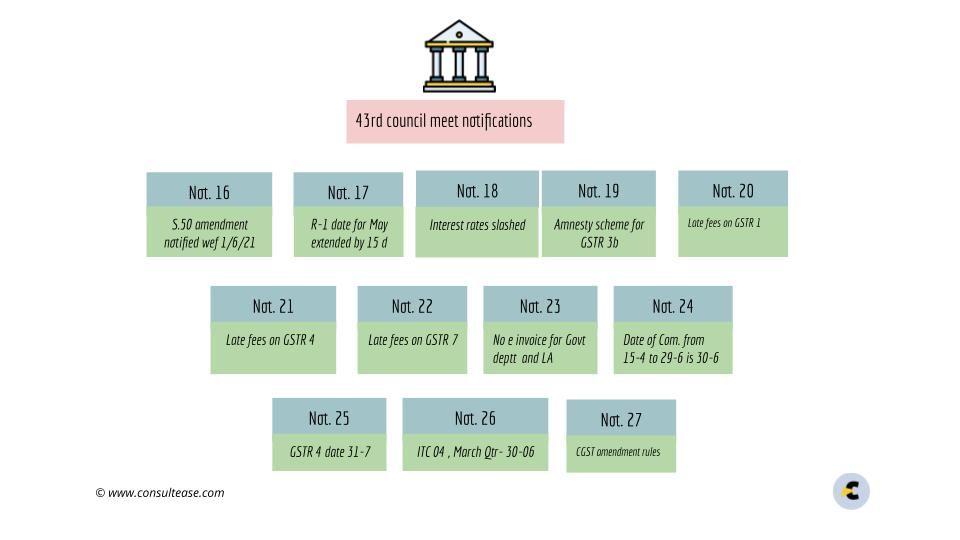

GST ComplianceTax Connect’s Analysis of Notifications To Give Effect To The Recommendations of 43rd GST Council Meeting Held On 28th May 2021

1. Relating To Real Estate – Notification No. 02/2021 – Central Tax (Rate) & Notification No. 03/2021 – Central Tax (Rate) In the 43rd Meeting of The GST Council, it was recommended to allow credit to landowners in joint development agreements even before the completion

GST Compliance

GST ComplianceImportant changes in GST Return, Interest and Rules

Not. 16/2021 Provisions of Section 112 of FA 2021 is notified applicable from 1st July 2017 112. In section 50 of the Central Goods and Services Tax Act, in sub-section (1), for the proviso, the following proviso shall be substituted and shall be deemed

GST Compliance

GST ComplianceBrief Synopsis of Amendments as Notified CBIC on 01.06.2021

Interest Liability on the amount paid through Electronic Cash Ledger shall be applicable retrospectively from 01.07.2017 Notification No. 16/2021 – Central Tax Section 112 of the Finance Act, 2021 shall be effective from 01.06.2021 As per Section 112 proviso shall be substituted and shall

GST Compliance

GST ComplianceNational Informatics Centre Release Notes: 01/06/2021

With reference Notification, 15/2021-CT dated 18.05.2021, to blocking of GSTIN for e-Way Bill generation is now considered only for the defaulting Supplier GSTIN and not for the defaulting Recipient or Transporter GSTIN. Click on the notification for more details. Mode of transport Ship is

GST Compliance

GST ComplianceNotification No. 26/2021 – Central Tax

Notification No. 26/2021 – Central Tax [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 26/2021 – Central Tax New Delhi,

GST Compliance

GST ComplianceNotification No. 25/2021 – Central Tax

Notification No. 25/2021 – Central Tax [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 25/2021 – Central Tax New Delhi,

GST Compliance

GST ComplianceNotification No. 24/2021 – Central Tax

Notification No. 24/2021 – Central Tax [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 24/2021 – Central Tax New Delhi,

GST Compliance

GST ComplianceNotification No. 27/2021 – Central Tax

Notification No. 27/2021 – Central Tax [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 27/2021 – Central Tax New Delhi,

GST Compliance

GST ComplianceNotification No. 21/2021 – Central Tax

Notification No. 21/2021 – Central Tax [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 21/2021 – Central Tax New Delhi,