How to file annual return: Practical guide

Table of Contents

Introduction:

How to file annual return? it is a buzzing question.The last date for filing of annual return is approaching fast. Even after the extension of 6 months, most the taxpayers have failed to understand it till now. That’s the reason we have drafted this write up on how to file an annual return? There are many modifications in its form. Here we have compiled a guideline on how to file annual return step by step.

Step 1: Calculate the relevant figures:

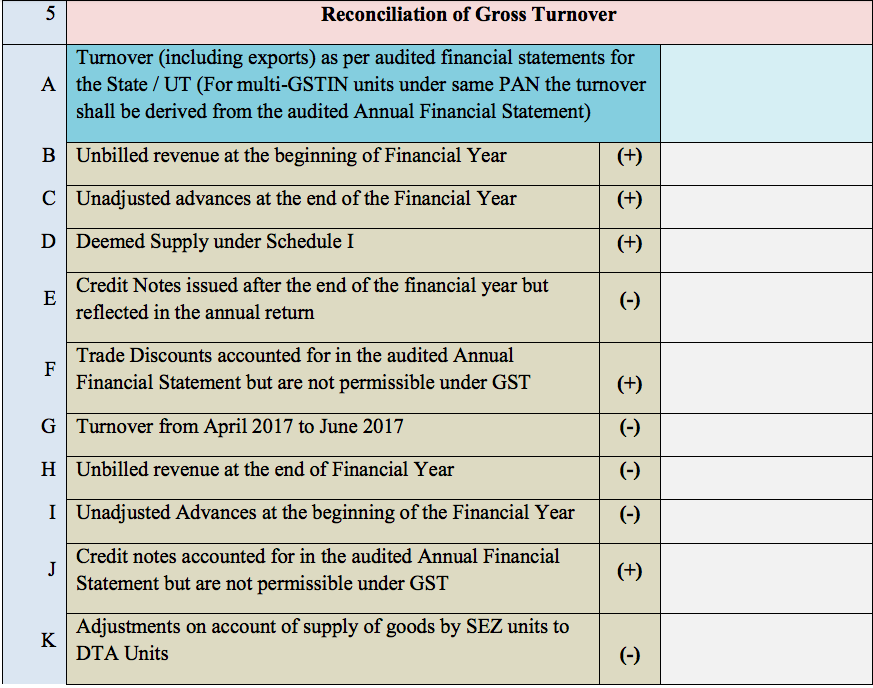

The first step towards the filing of annual return is to draft the correct data. An Annual return has the following type of data:

- All transactions are liable for payment of tax. It will include the

- purchases liable for RCM,

- outward supply and

- advances liable for GST.

- All outward transactions not liable for payment of tax. This amount will include the exempted, nil rated, non-GST and no supply.

The following table can be used to calculate the taxable figure:

Calculate the amount of liability for payment of tax:

Once you have calculated the amount liable for the payment of tax its easy to calculate tax. The formula to calculate it will be:

- Total amount liable for tax * Tax rate

This will be the amount of tax to be paid. It belongs to all the transactions for FY July 2017 to March 2018. The payment of this amount can be done via two items:

- Eligible ITC available in input tax credit ledger.

- The amount available in cash ledger

Ultimately the payment of liability shall be made via any of above. Now we need to understand what is eligible ITC. It is valid ITC taken by the taxpayer. It should fulfil the following conditions:

- Take all input tax credit on the purchase

Related Topic:

Annual Return: Section 92 of Companies Act, 2013

(-) Ineligible ITC:

(-) reversals:

(-) ITC for items used personally

(-) ITC wrongly taken:

The amount left after all of the above adjustment will be out eligible ITC>

Calculate the actual input tax credit eligible in the relevant period:

To be an eligible input tax credit, an amount is required to qualify the following two criteria

- It should be an eligible input tax credit under the provisions of section 16.

- ITC is claimed by the taxpayer in GSTR 3b within the prescribed time.

- It is not a blocked credit u/s 17(5)

- Reversal of rule 42 & 43 are made from it.

Step 2: Make a reconciliation with GSTR 3b where tax is payable

Table 9 and 14 of GSTR 9 contains the payment related information. In table 9 payment data will be auto-populated from GSTR 3b. This payment will be up to the return of March 2018.

In table 14 of GSTR 9, the payment data will be fed. GSTR 3b filed in this period may have taxes of the same period or previous period. If GSTR 1 is defective then actual data shall be relevant.

Step 3: Make the reconciliation of tax payable and tax actually paid:

The Following type of errors may be there even if overall figure matches.

- wrong ITC was utilized against a wrong liability.

- Instead of taking an ITC it was wrongly reversed.

- Tax paid in CGST & SGST via ITC but liability was of IGST or Vice versa.

We need to find out the correct figure for the tax liability. Then we need to verify whether it was correctly paid via eligible ITC and cash ledger. If not, then we need to mention the correct ITC and cash ledger figures. In case there is any shortage then it should be made good via DRC 03. Thus it will let the taxpayer correct all the errors.

Step 4: corrective actions:

Then a corrective action shall be taken. In case there is any excess payment of tax then refund shall be claimed. . Interest liability shall also be paid via challan.It’s not easy but a try is required. Now we understand How to file annual return.

Step 5: How to file annual return finally on the portal

Feed all of the above data on the portal. Before filing you need to click on calculate the fee. Only after that, you will be able to file it. Precautions are required before filing it.

CA