Latest Resources

| M | T | W | T | F | S | S |

|---|---|---|---|---|---|---|

| 1 | ||||||

| 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| 9 | 10 | 11 | 12 | 13 | 14 | 15 |

| 16 | 17 | 18 | 19 | 20 | 21 | 22 |

| 23 | 24 | 25 | 26 | 27 | 28 | |

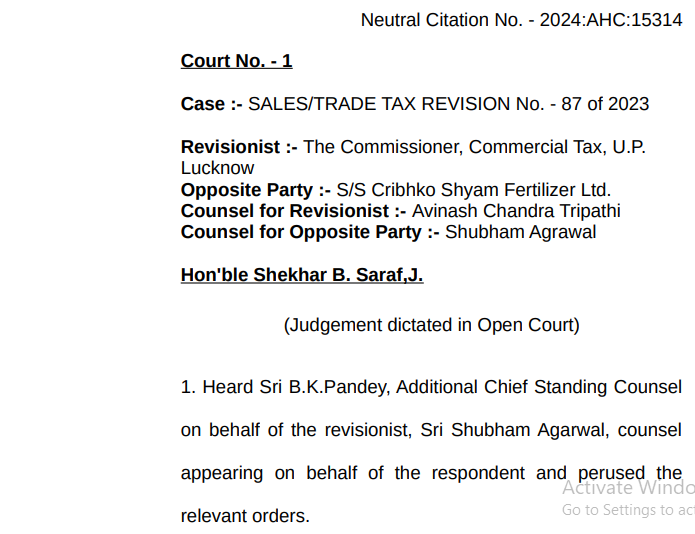

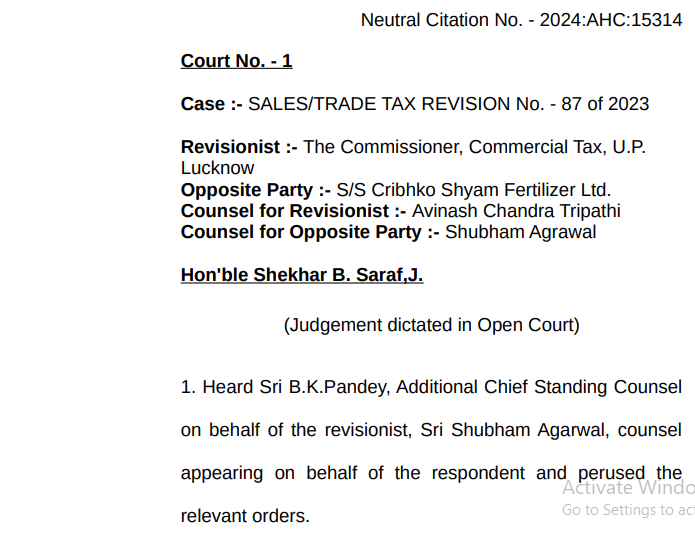

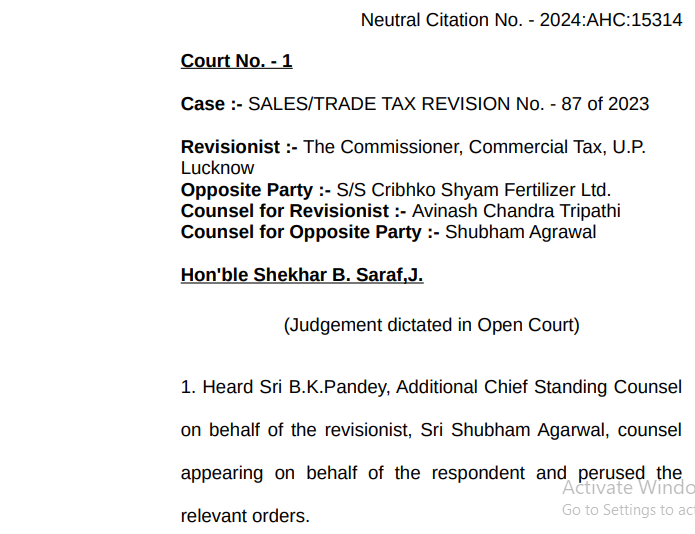

The Allahabad High Court ruled on a case involving the interpretation of Section 13(1)(f) of the Uttar Pradesh Value Added Tax Act, 2008 (UP VAT Act). This section pertains to the conditions under which input tax credit can be claimed by a registered taxpayer. Specifically, Section 13(1)(f) deals with situations where goods are sold at a price lower than the purchase price (in the case of resale) or cost price (in the case of manufacture), and it outlines the extent to which input tax credit can be claimed. In the case discussed, the respondent/assessee had been issued a show cause notice regarding deficiencies discovered during an investigation for the assessment year 2014-15. The explanation provided by the assessee regarding the low selling price of goods was deemed unacceptable, leading to the reversal of input tax credit under Section 13(1)(f) of the UP VAT Act. However, the first appellate authority quashed a disputed amount of the reversed input tax credit, which was challenged by the revenue department through a revision before the High Court. The revenue department argued that the benefit of input tax credit should be limited to goods purchased within the state of Uttar Pradesh on which VAT was paid, citing relevant sections of the UP VAT Act and the UP Value Added Tax Rules, 2008. The Tribunal, on the other hand, had already determined that the assessee had paid far more tax than the input tax credit claimed. Specifically, the Tribunal noted that the assessee had claimed input tax credit of Rs. 1,43,83,587, against which tax of Rs. 13,27,46,784 was deposited on the sale of manufactured urea. Due to this significant difference between the tax paid and the input tax credit claimed, the Tribunal concluded that Section 13(1)(f) was not applicable to the assessee. Justice Shekhar B. Saraf, upon reviewing the Tribunal’s findings and the record, affirmed that the assessee had indeed paid substantially more tax than the input tax credit claimed. As a result, the provisions of Section 13(1)(f) of the UP VAT Act were deemed not applicable to the assessee. Consequently, the revision filed by the revenue department was dismissed by the High Court, upholding the Tribunal’s decision in favor of the assessee

Recieve the most important tips and updates

Absolutely Free! Unsubscribe anytime.

We adhere 100% to the no-spam policy.