Interest on wrongly paid tax in GST: An analysis

Table of Contents

Wrongly paid tax in GST vis a vis interest

Place of supply is the base criteria to decide the nature of tax in GST. In many cases, we pay tax under the wrong head. How this wrongly paid tax will be treated? There may be various reasons for it.

- We may misjudge the nature of a transaction. e.g. Mr. X of Delhi supplied goods to Mr. Y of Delhi. Goods were delivered at the address of Mr. Z at Tamilnadu, at the order of Mr. Y. The accountant responsible for raising invoice misjudged Pos with the place of delivery. he raised the invoice of IGST. Whereas by virtue of section 10(b) of IGST Act it should be intrastate.

- The invoice was raised in CGST and SGST but at the time of filing of returns, the tax was paid in IGST head in 3b.

Coverage of section 77 of CGST Act

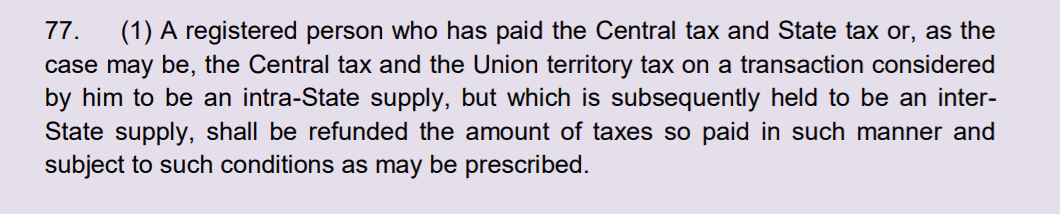

Section 77 of CGST Act covers this instance.

The text of the section is here.

Let us have a look at its literal interpretation. In case supply is held to be intrastate there will be no interest. The following conditions shall be fulfilled to get relief of no interest.

- There should be a misjudgement of the nature of supply. It should be due to the Place of supply wrongly determined.

- The supply shall be held to be intrastate in place of the interstate. (read vice versa for IGST)

Here it is important to understand the meaning of “held”. Grammatically it is the past and past participle of the hold. But legally we use it as a decision by adjudicating authority.

If we take this second meaning, it will result in a weird outcome. If I correct my misjudged supply myself, there will be interest. If an officer decides it, there will be no interest by virtue of section 77 of the CGST Act. This section is in chapter of demand and recovery. Thus this interpretation may hold good. But this will inspire the taxpayer to not to declare their mistake and wait for an adjudication.

Purposive and more logical shall be if we take its grammatical meaning. Even if the taxpayer arrives at the conclusion that he misjudged his supply earlier. He should be allowed to correct it without any interest.

When supply is correctly assessed but tax is paid wrongly:

Then there can be another scenario. The second case I discussed earlier. In this case, supply was correctly assessed but the tax was paid wrongly. Will this case also be covered by section 77? Whether he shall get the relief form interest payment in this case also? Because here the reason for payment to the wrong account is not the misjudgment of supply but the clerical error while filing the return.

In the case of Shree Nanak Ferro Alloys (P.) Ltd. v. Union of India, It was observed that even in this case interest shall not be there.

Disclaimer: It is just a view and shall not be construed as legal advice in any manner. No liability of the author or portal will be there. Please consult an expert before taking a stand.

CA