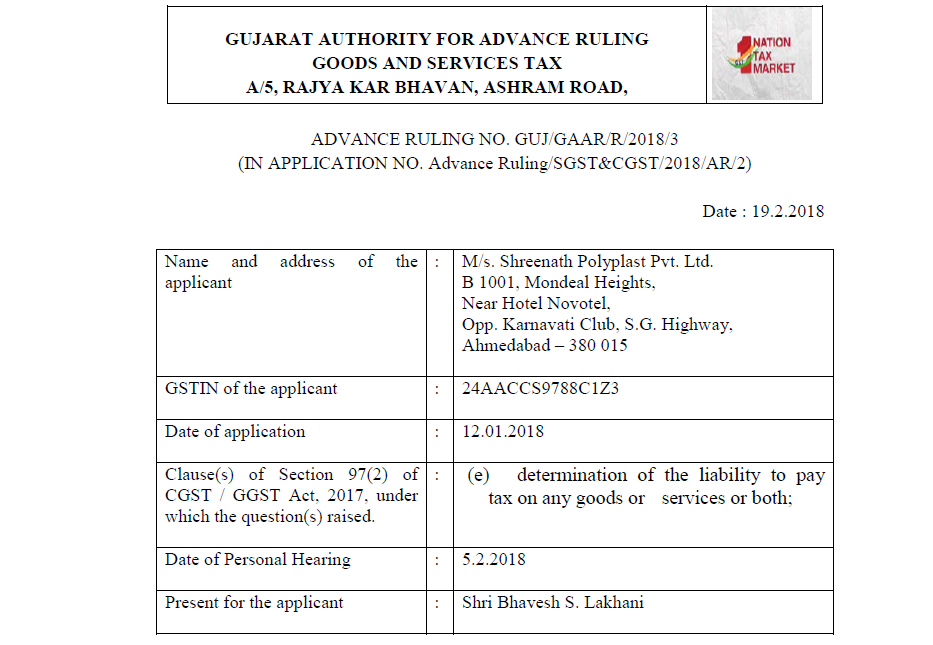

Original copy of GST AAR of M/s. Shreenath Polyplast Pvt. Ltd.

Original copy of GST AAR of M/s. Shreenath Polyplast Pvt. Ltd.

In the GST AAR of M/s. Shreenath Polyplast Pvt. Ltd. the applicant has raised the query regarding the applicability of GST on the interest charged on the short-term loan. The short-term loan was transaction based on the goods which are exempt under Notification No. 12/2017-CTR. Following is the GST AAR of M/s. Shreenath Polyplast Pvt. Ltd.:

Order:

The applicant, M/s. Shreenath Polyplast Pvt. Ltd. has raised the following questions for advance ruling –

“Whether an amount charged as interest on transaction-based short-term loan given by the Del Credere Agent (DCA) to buyers of material is exempt from tax in terms of the Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 (Serial Number 27)?

2.1 The applicant has submitted in the application for Advance Ruling that they are Del Credere Agent (herein after referred to as “DCA”) appointed by the supplier of goods (herein after referred to as “principal”) and has dual role, the first role is to promote the sale and take orders for goods to be supplied by the principal directly and the second role is to guarantee the principal for the payment of goods supplied. If customers fail to make payment, DCA is required to make the payment to the principal. Normally, Principal takes Bank Guarantee (BG) and / or Security Deposit against which principal assigns certain limit to the DCA in their system. Within that limit, DCA is allowed to place orders of the customers. At the end of the month, for the orders booked through such DCA and goods supplied by the principal, DCA gets the commission from principal for which DCA raises invoices on the principal along with GST.

2.2 The applicant clarified that the role of the DCA is limited to order booking and ensuring payment to the principal in case of default from the customer. In the entire transaction, neither principal supplies the goods to DCA, nor does DCA supply the goods to customers. Goods are directly supplied by Principal to the customers at the price declared by the principal from time to time by charging applicable GST on the invoice. On the due date, the customer pays to principal directly for the material supplied to them. In case of any delay in payment from the customer, principal charges interest along with GST.

2.3 The applicant reiterated that the role of the DCA is limited to order booking and guaranteeing payment. Supply of material is directly by the principal to the customer. Any delay in supply or any quality issue, it is principal who directly compensates the customer. DCA does not buy, store or sale any material of principal to any customer and therefore there is no transaction of any purchase or sale of goods in his books.

2.4 It is submitted that in the entire transaction, the maximum interaction buyer of the material has with DCA. Due to this, on some occasions, when the buyer is not in a position to pay to principal on the due date, he approaches DCA to extend short term loan and the loan is extended by the DCA by making payment to the principal on behalf of the customer. The loan is repaid to DCA by the customer along with agreed interest. The rate of interest on such short term transaction based loan (from 10 days to 90 days) is as mutually agreed between buyer of the material and DCA. Sometimes, customer does not make payment to the DCA and gives Letter of Credit (LC) for 60 / 90 days, which DCA gets discounted with the bank. In this transaction also, interest is payable for the period until LC is discounted. For interest, DCA raises debit notes on the customers. Customer pays interest while repaying the loan amount. Such interest payments are subject to TDS in terms of Income Tax Act.

2.5 It is further submitted that normally principal does not continue supply to customer until pending bills are paid by the customer. By following above process, since customer is able to arrange finance by taking short term transaction loan from the DCA, the principal gets the payment and customer gets the un-interrupted supplies.

2.6 In respect of above commercial practice, the aforesaid question has been raised for advance ruling.

Download the GST AAR of M/s. Shreenath Polyplast Pvt. Ltd. by clicking the below image:

3.1 The applicant submitted that the amount charged by DCA as interest from the buyer of the materials is not liable to tax in terms of Sr. No. 27 of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017.

3.2 The applicant further submitted that DCA is giving the loan to the buyer and charging the interest thereon from them and accordingly it will be covered under item at serial number 27 of the table attached to the impugned Notification and therefore, no tax would become payable on the amount charged as interest.

3.3 The applicant referred to Section 15(2)(d) of the Central Goods and Services Tax Act, 2017 (herein after referred to as the ‘CGST Act, 2017) and submitted that the said provision does not apply to the facts of the present matter. They submitted that in the present case, in the commercial practice as explained earlier, DCA is not supplying any goods to the customer but it is the principal who is directly supplying the goods to the customers. Thus, interest charged by DCA from customers is not for delayed payment of consideration of any underlying supply but said interest is charged towards loan given to the customers and hence such interest will be covered under item 27 of the table attached to the impugned notification.

4. State Tax, GST Cell has given its opinion as under :-

“The Del Credre agent receives higher commission because he ensures paymet to the supplier. Whether the agent extends a loan to the buyer for making payment to the supplier or whether the agent himself makes payment on behalf of the buyer, no amount towards this shall be added to the price and GST will be leviable only on the consideration for supply of goods (on the supplier) and the commission payable to the agent (on the agent).”

5. We have considered the submissions made by the applicant in their application as well as at the time of personal hearing.

6. The issue involved is whether an amount charged as interest on transaction based short term loan given by the applicant, working as Del Credere Agent (DCA), to buyers of material, is exempt from Goods and Services Tax in terms of Sl. No. 27 of the table to Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017, or otherwise .

7. In the case of transaction of supply of goods through DCA, the principal supplies the goods to and receives payment from the customers. In case of failure of customer to make payment, the DCA makes payment to the principal. The DCA gets the commission from principal. It is submitted by the applicant that when the buyer is not in a position to pay to principal on the due date, he approaches the DCA, who extends short term loan by making payment to the principal on behalf of the customer and the loan is repaid to DCA by the customer along with agreed interest. It is also submitted that sometimes, customer does not make payment to the DCA and gives Letter of Credit for 60 / 90 days, which DCA gets discounted with the bank and in this transaction also, interest is payable for the period until Letter of Credit is discounted. For interest, DCA raises debit notes on the customers and customers pay interest while repaying the loan amount.

8. We find that the extension of loan by the applicant (DCA) to the customers is a transaction separate from the transaction of supply of goods by the principal to the customers against consideration wherein the applicant (DCA) also gets the commission from the principal. The issue before us is limited to examine whether interest received by the DCA towards extension of loan to the customers is covered by Sl. No. 27 of the Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017, or otherwise.

9.1 Section 15(2)(d) of the CGST Act, 2017 and the Gujarat Goods and Services Tax Act, 2017 provides as follows :-

“15. Value of taxable supply. — (1) ……

(2) The value of supply shall include —

(a) ……

(b) ……

(c) ……

(d) interest or late fee or penalty for delayed payment of any consideration for any supply; and

(e) ……”

9.2 We find that the interest received by the applicant is consideration towards loan extended to the customers and such interest is not towards the payment of consideration for supply of goods by the principal to the customers, which, as we have already observed, is a separate transaction.

10.1 Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017, as amended, provides exemption to supply of various services, as specified in column (3) of the table to the said Notification. Sl. No. 27 of the table to the said Notification provides as follows:-

TABLE

| (1) | (2) | (3) | (4) | (5) |

| Sl. No. | Chapter, Section, Heading, Group or Service Code (Tariff) | Description of Services | Rate (percent) |

Condition |

| 27 | Heading 9971 | Services by way of— (a) extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount (other than interest involved in credit card services); (b) inter se sale or purchase of foreign currency amongst banks or authorized dealers of foreign exchange or amongst banks and such dealers. |

Nil | Nil |

10.2 As per the aforesaid Sl. No. 27 of the table to Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017, services by way of extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount (other than interest involved in credit card services) is exempt from payment of Goods and Services Tax. As in the transaction of extension of loan by the applicant, the consideration is received by way of interest, the same is covered by the aforesaid Sl. No. 27 of the table to Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017, and hence exempted from payment of Goods and Services Tax.

Ruling:

11. In view of the foregoing, we rule as under –

Service provided by M/s. Shreenath Polyplast Pvt. Ltd. (GSTIN 24AACCS9788C1Z3) by way of extending short-term loans in so far as the consideration is represented by way of interest, is covered under Sl. No. 27 of the Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 and Notification No. 12/2017-State Tax (Rate) dated 30.06.2017, and hence exempt from payment of Goods and Services Tax.

Consultant