Original copy of GST AAR of SHREE CONSTRUCTION

Original copy of GST AAR of SHREE CONSTRUCTION

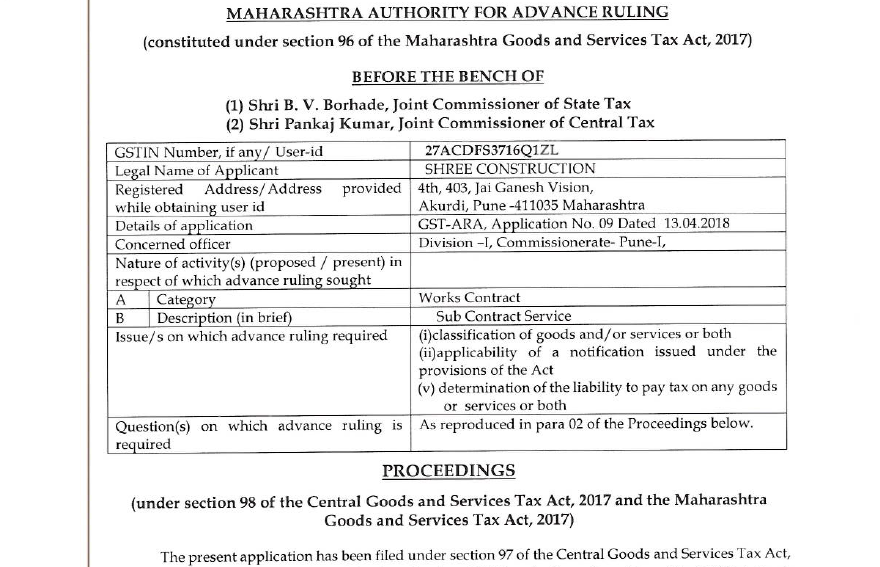

In the GST AAR of Original copy of GST AAR of SHREE CONSTRUCTION. The applicant has raised the query regarding the tax rate applicable on the Works Contract Services. Following is the order passed by the GST AAr for the case of SHREE CONSTRUCTION:

PROCEEDINGS

The present application has been filed under section 97 of the Central Goods and Services Tax Act, 2017 and the Maharashtra Goods and Services Tax Act, 2017[hereinafter referred to as “the CGST Act and MGST Act”] by SHREE CONSTRUCTION, the applicant, seeking an advance ruling in respect of the following questions :

1. What Tax rate to be charged by the sub-contractor to main contractor on Works Contract Services WCS) pertaining to railways original works contract?

2. Whether to charge tax rate of 12% GST or 18% GST?

At the outset, we would like to make it clear that the provisions of both the CGST Act and the MGST Act are the same except for certain provisions. Therefore, unless a mention is specifically made to such dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provision under the MGST Act. Further to the earlier, henceforth for the purposes of this Advance Ruling, a reference to such a similar provision under the CGST Act / MGST Act would be mentioned as being under the “GST Act”.

2. FACTS AND CONTENTION – AS PER THE APPLICANT

The submissions, as reproduced verbatim, could be seen thus-

Statement of relevant facts having a bearing on the question(s) raised

1. We are providing works contract service as sub-contractor to main contractor for original contract work pertaining to railways.

2. As per Notification No-20/2017- Central Tax (Rate) dated 22-08-2017 the ratetT GS’ is 12% for composite supply of works contract supplied by way of construction, erection, commission or installation of original works pertaining to railways.

3. As per SR.No-12 in press release of 25th meeting of GST council held at New Delhi on 18-01-2018, the rate of GST applicable to main contractor should be levied by sub-contractor.

4. As per Notification No-01/2018- Central Tax( Rate) dated 25-01-2018 the service provided by sub- contractor to main contractor for railway original works contract services is not specified in the notification.

Statement containing the applicant’s interpretation of law and/or facts, as the case may be, in respect of the afore said question(s) (i.e. applicant’s view point and submissions on issues on which the advance ruling is sought)

1. As per our view point even though we are sub-contractor providing service to main contractor for original contract work pertaining to railways, we should charge 12% GST only and not 18% as applicable in other cases.

2. The contract for original works pertaining to railways remains the same works contract.

3. As there is difference of opinion after reading of press release of 25th meeting of GST council dated 18-012018 and notification No 1/ 2018 dated 25-01-2018, we are not in position to levy correct rate of GST on original sub-contracting work pertaining to railways carried on by us for our main contractor.

4. This advance ruling is sought clarification for rate of tax to be levied by the sub-contractor to main contractor for original contract work pertaining to railways.

Further submissions, as reproduced verbatim, could be seen thus-

Our Submission is in Part 1 and Part 2 hereunder –

1. Part 1 – The Issue put before your honour.

2. Part 2 – The submission and explanation in support of our issue.

Download the original copy of GST AAR of SHREE CONSTRUCTION. By clicking the below image:

Part 1: Issue

a. We are a Works Contractor.

b. We execute and undertake composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017.

c. We have been awarded a subcontract by another works contractor to execute the original work of civil construction for Railways.

d. As per the schedule of GST rate for a service under GST, the composite value of works contract is classified along with rates of tax as hereunder.

Extract of classification of services

Section 5 Construction Services

| SAC Code | Description of Services | Rate in % |

| 9954 | (v) Composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017, supplied by way of construction, erection, commissioning, or installation of original works pertaining to,- (a) railways, excluding (including substituted from 25/01/2018)) monorail and metro; (b) a single residential unit otherwise than as a part of a residential complex; (c) low-cost houses up to a carpet area of 60 square metres per house in a housing project approved by competent authority empowered under the Scheme of Affordable Housing in Partnership’ framed by the Ministry of Housing and Urban Poverty Alleviation, Government of India; (d) low cost houses up to a carpet area of 60 square metres per house in a housing project approved by the competent authority under- (1) the Affordable Housing in Partnership component of the Housing for All (Urban) Mission/Pradhan Mantri Awas Yojana; (2) any housing scheme of a State Government; (e) post-harvest storage infrastructure for agricultural produce including a cold storage for such purposes; or (f) mechanised food grain handling system, machinery or equipment for units processing agricultural produce as food stuff excluding alcoholic beverages, | 12 |

e. The sub-contractor providing services to main contractor is further classified only under two categories as under

| SAC Code | Description of Services | Rate in % |

| 9954 | (ix) Composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017 provided by a sub-contractor to the main contractor providing services specified in item (iii) or item (vi) above to the Central Government, State Government, Union territory, a local authority; a Governmental Authority or a Government Entity. Provided that where the services are supplied to a Government Entity, they should have been procured by the said entity in relation to a work entrusted to it by the Central Government, State Government, Union territory or local authority, as the case may be. | 12 |

| (x) Composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017 provided by a sub-contractor to the main contractor providing services specified in item (vi) d above to the Central Government; State Government, Union territory, a local authority, a Governmental Authority or a Government Entity. Provided that where the services are supplied to a Government Entity, they should have been procured by the said entity in relation to a work entrusted to it by the Central Government; State Government, Union territory or local authority, as the case may be. | 12 |

f. Even though, we being subcontractor providing civil construction services to main contractor effecting original works contract for Railways which is not covered in 9954 (ix) and 9954 (x), we believe that the rate applicable to us. is 12% only which is the rate applicable for Composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017, supplied by way of construction, erection, commissioning, or installation of original works pertaining to,- (a) railways excluding(including substituted from 25/01/2018) monorail and metro;,

Thus, to have certainty in the tax liability in relation to an activity provided by us, our application for Advance Ruling is sought for

1. At what rate of tax the liability should be determined on services provided by us to main contractor effecting civil construction work for railways?

2. Under which head we should classify our Services to execute civil construction contract for railways?

Part 2: Our Submission and Explanation

In support of our charging tax @ 12%, we submit our submission as under –

1. As per the section 2 (119) of the CGST Act, 2017 “works contract” means a contract for building, construction, fabrication, completion, erection, installation fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property, wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract;

2. As per Section 2 (5) of CGST Act, 2017 “agent” means a person, including a factor, broker, commission agent, arhatia, del credere agent, an auctioneer or any other mercantile agent; by whatever name called, who carries on the business of supply or receipt of goods or services or both on behalf of another;

3. Contractor and sub-contractor are not defined under the CGST Act, 2017 but as per the general definition

a. Contractor means a person or firm that undertakes a contract from the employer to provide materials or labour to perform a service or do a job at a specified price.

b. A subcontractor means a person who is hired by a general contractor (or prime contractor, or main contractor) to perform a specific task as part of the overall project or the total project at a specified price for services provided to the project by the originating employer.

4. When the contractor awards either wholly or partially, the contractual obligation to a sub-contractor the contracts remains the same and the identity of the contract doesn’t change.

5. When the contractor awards either wholly or partially, the work to the subcontractor, the work to be performed by the contractor as well as subcontractor remains same and identical to what is specify in the contract between the main contractor and the employer.

6. It can also be seen from the definition quoted above that subcontractor is not doing anything other but only what is specified in the contract between the main contractor and the employer.

7. As per the definition of agent above a agent is a person who carries on the same business of supply and / or receipt of goods or services or both on behalf of another. Thus we can call a subcontractor as an agent also who is undertaking the same supply of service for main contractor.

8. It can also be said that, the sub-contractor is only an agent of the contractor and the works job undertaken by him passes directly from the sub-contractor to the employer.

9. As the work get transferred directly to the employer by the subcontractor the works contract remains the same and therefore leads to the conclusion that there is only one contract which is undertaken by the contractor as well as subcontractor.

10. In our case, it is the transaction of a works contract, where the property in goods passes directly to the employer as and when we as a subcontractor have transferred and put our material and services for of execution of civil work carried for railways. The main contractor cannot take out our executed job and cannot treat it separately. Thus it cannot be said at any point of time, that the property in the works job passes to the contractor where the work is executed by us a subcontractor.

11. As we have already noticed, we are only an agent of the contractor and the property in goods passes directly from us being subcontractor to the employer which leads us to the conclusion that there is only one contract that is between railways and contractor as well as subcontractor. And we are doing the job for railways.

12. We would also like to highlight the intent of the Government is to bring the rates of main contractor and subcontractor at par while they are providing their services to Central Government, State Government, Union territory, a local authority, a Governmental Authority or a Government Entity.

13. Railways being a Governmental Authority / Entity is already covered under clause (x) of heading 9954 of section 5 of classification of services even though not specified separately.

14. Thus the rate applicable for civil works contract carried out for railways in para (v) of heading 9954 of section 5 of classification of services should be applicable to subcontractor also.

03. CONTENTION – AS PER THE CONCERNED OFFICER

2. As directed the application has been examined with reference to provisions of Chapter XVII of CGST Act, 2017 and it is submitted that –

i) Prima facie it appears that the question on which the advance ruling is sought under CGST Act doesn’t fall under any of the category mentioned in sub section (2) of Section 97 of the Act as the question, put forth by the Applicant is only relating to charging of rate of tax on the Works Contract Services (WCS) by the sub contractor to n contractor in respect of railways original works contract.

ii) On examination of the Notification No.20/ 2017-Central Tax (Rate) dated 22.08.2017 it appears that in terms of serial number (v) of Table, Composite supply of works contract as defined in clause (119) of Section 2 of CGST Act, 2017, supplied by way of construction, erection, commissioning or installation of original works pertaining to – (a) railways, excluding monorail and metro; fate of tax is prescribed as 12%. Other than these services, rate of tax is prescribed at the rate of 18% as shown in serial number (vi). There is no Specific inclusion of WCS services provided by sub contractor to main contractor. Therefore, it appears from the said Notification No.20/ 2017Central Tax (Rate) dated 22.08.17 that the category of WCS services provided by sub-contractor to main contractor are not covered by the said notification.

(iv) As per amending Notification No.01 /2018-Central Tax (Rate) dated 25.01.2018, in para (C) it is substituted that in serial number (ix) and (x) that for Composite supply of WCS provided by subcontractor to main contractor specified in item (iii) or item (iv) to the Government Entity, rate of tax prescribed is 12%. However, for construction services other than (v), rate of tax is prescribed as 18%.

Therefore, Notification No.01/2018-Central Tax (Rate) dated 25.01.2018, the services provided by sub contractor to main contractor for railway original works contract services are excluded from the main entry (ix) and (x) of the said notification. All other construction services other than specified services are therefore attract rate of 18% tax which includes services provided by sub contractor to main contractor for railway original works contract.

(v) The contention of the Applicant, that their services are covered by the original works contract specified in para (ix) and (x) of amended Notfn.No.01/2018-CT(Rate) dated 25.01.2018, is not correct in as much as the said Notification has classified all other Works Contracts relating to Construction services in head (xii) prescribing rate of 18%. The minutes of meeting dated 18.01.2018 para-12 quoted by the Applicant has mention of Government Entity but doesn’t specifically include WCS provided by sub contractor to main contractor in relation to Railways.

In view of above, the question before the Advance Ruling Authority may be disposed off as per above provisions of law for the time being in force without accepting the interpretative views of the Applicant based on the minutes of meeting dated 18.01.2018 quoted by them.

04. HEARING

The preliminary Hearing was held on 12.06.2018. Shri Deepak Chandok, Chartered Accountant, duly authorized along with Ms Veena Chandok, CA., appeared and requested for admission of application as per details in ARA. No jurisdictional officer from the side of the department was present.

The application was admitted and Final Hearing in the matter was held on 03.07.2018. Shri Deepak Chandok, Chartered Accountant, along with Shri Vasant Hidakar, Partner appeared and made oral and further written submissions which were taken on record. The jurisdictional officer, Sh. Devender Bakliwal, Supdt., Division-I, Pune-I Commissionerate appeared and made written submissions which were taken on record .

05. OBSERVATIONS

We have gone through the facts of the case, submissions made by the applicant and the department and documents on record.

The applicant has submitted that they are supplying Works Contract Services (WCS), as a subcontractor, to the main contractor who in turn are supplying WCS for original work pertaining to the Railways. They have made further submissions that when a contractor awards either wholly or partially, the work to a sub-contractor, then the work to be performed by both of them remains the same and identical to what is specified in the contract between the main contractor and the employer, in this case, the Railways and as per Notification No-20/2017- Central Tax (Rate) dated 22-08-2017 the rate of GST is 12% for composite supply of works contract supplied by way of construction, erection, commission or installation of original works pertaining to railways. They are claiming that since the tax rate is 12% for the main contractor, the same rate should be applicable to them too. They have also submitted that Notification No-01/2018- Central Tax( Rate) dated 25-01-2018 has made certain amendments to the earlier Notification No. 20/2017 but has not provided clarification with respect to services provided by subcontractor to the main contractor for railway original works contract services. They have also cited SR.No-12 in the press release of the 25th meeting of GST council held at New Delhi on 18-01-2018 and stated that the rate of GST applicable to the main contractor should be levied by sub-contractor.

We find that Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017 has specified the rate of central tax to be levied on Intra State supply of services of a description specified in Column 3 of the Table in the said Notfn, falling under the scheme of classification of services mentioned therein. The relevant clauses (v) as mentioned by the applicant in their favor, of the said Notfn, as amended by Notfn No. 20/2017-Central Tax (Rate) dated 22.10.2017 is reproduced below:-

| S1 No. | Chapter, Section or Heading | Description of Service | Rate

(percent) |

Condition |

| 3 | Heading 9954 (Construction services) | (v) Composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017, supplied by way of construction, erection, commissioning, or installation of original works pertaining to,-

(a)railways, excluding monorail and metro; (b) ………………………………………………. ; (c) ……………………………………………….. ; (d) ………………………………………………. ; (e) ……………………………………………. ; or (f) ………………………………………………. |

6 | -] |

A plain reading of Sr. No. 3, clause (v) reveals that ‘composite supply of WCS supplied by way of construction, erection, commissioning, or installation of original works pertaining to,-

(a) railways

attracts a tax rate of 6% each of CGST and SGST.

Here we may mention that the applicant has submitted that they have been sub-contracted by the main contractor to supply WCS and in turn, the main contractor is supplying WCS to the Railways. From the submissions made by the applicant, it appears that the WCS provided by them is the same or a part of the main contract entered into between the main contractor and the Railways. It also appears that works contract service is civil works performed by the sub-contractor for the Railways and the property in goods (materials used in the supply of Works Contract Service) also gets transferred to the Railways directly. In such a case as per the abovementioned clause (v) of Notfn No. 20/2017-Central Tax (Rate) dated 22.10.2017, the works contract service provided by the sub-contractor to the main contractor would be supply of Works Contract pertaining to Railways and therefore chargeable to tax @ 12% (6% of CGST and SGST each). However, the benefit of 12% tax rate would be available to the applicant only if the Works Contract Services provided by them are Composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017, supplied by way of construction, erection, commissioning, or installation of original works pertaining to railways.

Thus in respect of Sr. No. 3 of Notification No. 11/2017 dated 28.06.2017 as amended up till today, even the sub-contractor providing services of composite supply of works contract in respect of original works pertaining to railways would be covered for concessional rate of GST @ 12% as given under Sr. No. 3 of Notification No. 11/2017 as amended referred above.

06. In view of the deliberations as held hereinabove, we pass an order as follows:

ORDER

( under section 98 of the Central Goods and Services Tax Act, 2017 and the Maharashtra Goods and Services Tax Act, 2017)

NO.GST-ARA- 09/2018-19/B-65 Mumbai, dated. 11/07/2018

For reasons as discussed in the body of the order, the question is answered thus –

Q. No. 1: What Tax rate to be charged by the subcontractor to main contractor on Works Contract Services (WCS) pertaining to railways original works contract?

Answer: The tax rate to be charged by the sub-contractor to the main contractor would be @ 6% of CGST and SCSI each, in the present case.

Q. No. 2: Whether to charge the tax rate of 12% GST or 18% GST?

Answer: The tax rate to be charged would be 12% in the present case

Source: GST AAR Maharastra

Consultant