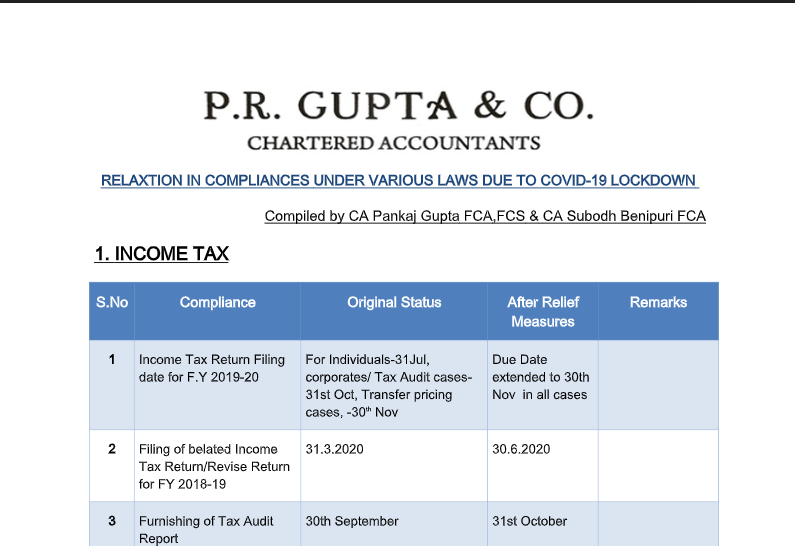

Relaxation in Compliances Under Various Laws Due To COVID-19 Lockdown

Table of Contents

Relaxation in Compliances Under Various Laws Due To COVID-19 Lockdown

1. Income Tax

| S.No | Compliance | Original Status | After Relief Measures |

Remarks |

| 1 | Income Tax Return Filing the date for F.Y 2019-20 |

For Individuals-31Jul, corporates/ Tax Audit cases- 31st Oct, Transfer pricing cases, -30th Nov |

Due Date extended to 30th Nov in all cases |

|

| 2 | Filing of belated Income Tax Return/Revise Return for FY 2018-19 |

31.3.2020 | 30.6.2020 | |

| 3 | Furnishing of Tax Audit Report |

30th September | 31st October | |

| 4 | Furnishing of Transfer Pricing Report |

31st October | 31st October | No Change |

| 5 | Time Limitation for Payment u/s 80(c)/ 80CCB/80CCD/80(D)/80E/ 80G for FY 2019-20 |

31.3.2020 | 30.6.2020 | |

| 6 | The time limit for Investment u/s 54EC/54/54F.e from Sec 54 to 54GB |

As prescribed | If time limitation is expiring between 20.3.20 to 29.6.20, then extended till 30.6.2020 |

|

| 7 | Period of stay in India for POI for determining residential status for FY 2019-20 |

The actual period of stay in India | From 22 nd March to 31 st March will not be counted |

Lockdown period should not be counted for the FY 2020-21 but no relaxation so far |

| 8 | Filing of Statement of Financial transactions ( Form 61A) |

31st May 2020 | 30th June 2020 | |

| 9 | Filing of Statement of Reportable Accounts ( Form 61B) |

31 st May 2020 | 30th June 2020 | Not specifically clarified but should be this position only |

| 10 | Time Limitation for giving reply to Notices, Appeal etc. |

As per existing limitation | Where the limitation is falling between 22 Mar to 29 Jun, last date shall be taken as 30th June |

|

| 11 | Application for Registration/Re- registration for charitable societies |

As applicable | If time limitation is expiring between 20.3.20 to 29.6.20, then extended till 31.12.2020 |

|

| 12 | Time Limit for Starting SEZ operations u/s 10AA |

If expiring by 31.3.2020 | Extended till 30.6.2020 |

If the letter of approval already issued up to 31.3.2020 |

| 13 | Time barring of Assessments |

31.3.20 / 30.9.20 / 31/12.20 | Extended by 3 months respectively |

|

| 14 | Interest on delay in Payment of Advance Tax, Self-Assessment Tax, Regular Tax, Equalization Levy, STT/CTT |

Tax Due Date falling between 20.3.20 to 30.6.2020 |

Interest shall be levied at @ 9% instead of 12% for the period 20.3.2020 till 30.6.2020 |

Provided Payment is made till 30.6.2020 |

| 15 | Advance Payment Tax Dates for FY 2020-21 |

Due Dates 15th June 15th September 15th Dec 15th Mar |

for 15th June installment, Concessional Interest @ 9% instead of 12% till 30.6.2020 |

Applicable only if Payment of tax is made till 30.6.2020 |

| 16 | Payment under Vivad Se Vishwas Scheme Without additional Interest |

30.06.2020 | Can pay till 31.12.2020 |

|

| 17 | Pending refunds for Assesses other than Corporates |

As per Applicable dates | Immediate refunds to be made |

2. Tax Deducted / Collected at Source ( TDS/ TCS)

| S.No | Compliance | Original Status | After Relief Measures |

Remarks |

| 1 | TDS/TCS Rates in Non Salary cases |

Professional-10%, Technical Fees-2% Rent-10%/2% Contractor-2%/1%, Brokerage/Commission-5% TDS immovable property-1% TDS on Payment of Rent> 50K p.m—5% Payment to contractor/ professional above 50 Lacs in case of Non business entity…1% |

For all deductions made between 14.5.20 to 31.3.2021, rates will be 75% of original Rate. |

This relief is only in No reduction in |

| 2 | All TDS/TCS returns for Q-4 of FY 2019-20 |

TDS …31.05.2020 TCS….15.05.2020 |

30.06.2020 | |

| 3 | Statement in Form 26QB/26QC/26QD including for Payment |

Feb20…30.3.20 Mar20… 30.4.20 Apr20…30.5.20 |

Extended till 30.06.2020 |

|

| 4 | Issue of TDS Certificates |

16,16A . Q-4 /19-20—15.6.2020 16B, 16C, 16D…… for March…15 th May For April…14 th June |

Extended till 30.06.2020 |

|

| 5 | Interest on delayed payment of TDS for the period 20.3.2020 to 30.2020 |

Non deduction: 1% p.m. Non -payment: 1.50% p.m. |

0.75 % on Non- payment if paid till 30.6.20 |

No penalty /prosecution if deposited by 30.6.20 |

| 6 | Form 15G/15H for FY 2020-21 ( If already have certificate for FY 2019-20) |

Submit before the deduction date. | Existing Certificate will apply up to 30.6.2020. But only if apply for FY 2020-21 up to 30.6.2020 |

if no certificate submitted for FY 2019-20, then no relief. |

| 7 | Certificate u/s 197 for Lower Rate of TDS/TCS (other than Non-Resident) ( If already have certificate for FY 2019-20) |

Applicable after receipt of certificate |

Existing Certificate will apply up to 30.6.2020. But only if apply for FY 2020-21 up to 30.6.2020 |

if no certificate issued for FY 2020- 21 & no certificate for FY 2019-20, then no relief. |

| 8 | Applicability of certificate u/s 197 for Lower Rate of TDS/TCS for Non- Resident) u/s 195 |

Applicable after receipt of certificate |

Existing certificate for FY 2019-20 will apply up to 30.6.2020 if same nature of transaction. But only if apply for FY 2020-21 up to 30.6.2020 |

No certificate for FY 2019-20, but certificate for FY 2020-21 applied but not issued, then 10% plus surcharge plus Cess if Non- Resident having PE in India |

| 9 | Procedure for Application u/s 197/209C(9) |

To be filed through TRACES Portal with DSC |

Can be filed through Email to Assessing Officer by filing Form 13 |

To Resend info on email to A.O where application for FY 2020-21 already made through E- portal. |

3. Goods & Service Tax (GST)

| S.No | Compliance | Original Status | After Relief Measures |

Remarks |

| 1 | GSTR-1 | Applicable original dates | No extension of due date but for Levy of Interest and late fees for Mar, Apr, & May 20 and Last Qtr return for FY 2019- 20, date extended till 30th June |

However, no levy of Late fees, if filed till the extended date, otherwise levy from day 1 of original due date |

| 2 | GSTR- 3B For Taxpayers up to Turnover up to 1.5 Cr in preceding FY |

Applicable original dates | For Feb—30th June For-Mar—3rd jul For Apr… 6th jul For May—12/14th July |

No Interest and Late fees if filed in Extended Time |

| 3 | GSTR- 3B For Taxpayers Turnover>1.5 crores but up to 5 Cr |

Applicable original dates | For Feb—29th June For-Mar—29th June For Apr… 30th June For May—12/14th July |

No Interest and Late fees if filed in Extended Time. |

| 4 | GSTR- 3B For Taxpayers having Turnover >5 Cr |

Applicable original dates | For Feb—24th June For-Mar—24th June For Apr….. 24th June For May— 27th June No Late fees if filed in Extended Time |

If filed within extended due Interest NIL up to 15 days of original due date and thereafter at Concessional Rate of 9% p.a |

| 5 | GSTR-5,6,7,8 | Applicable original dates | 30th June,20 | |

| 6 | GSTR-9 & 9C For Fy 2018-19 |

30th June,20 | 30th Sept20 | |

| 7 | E-Way Bill | Generated on or before 24th March and Expiring between 20th March to 15th April…as prescribed |

In this case the expiry of the E waybill shall be deemed to be extended till 31 st May 2020. |

|

| 8 | Composition Scheme | As per applicable dates |

Can be opted till 30 th June |

Should not file Returns for first Qtr of FY 2020-21 |

| 9 | Electronic Cash Ledger | The transfer was not possible |

Can file PMT-09 for |

|

| 10 | Filing of LUT for FY 2020- 21 |

Before the supply of export services without payment of GST |

Can be filed till 30th |

|

| 11 | DSC for GST Return-3B |

Required in Corporate & LLP Cases |

Not required, can be |

No relaxation for GSTR-1 |

| 12 | Revival of GST Registration Cancelled till 14.3.20 |

Where cancelled due to |

Application for |

|

| 13 | New GST Registration by IPR/RP |

20 th April,20 |

30th June,20 or within |

|

| 14 | Input GST credit – restriction rule of 110% with reference to GSTR2A |

Feb to Aug20 |

Relaxation given |

However, FORM GSTR-3B for Sept. 2020 shall be furnished with the cumulative adjustment of input tax credit |

| 15 | Payment under Sabka Vishwas Scheme |

31.3.2020 |

Extended till |

4. Companies Act / MCA Filings

| S.No | Compliance | Original Status | After Relief Measures |

Remarks |

| 1 | Audit under Companies Act for FY 2019-20 |

29th Sept 2020 (with Short Notice ). |

No relaxation so far | |

| 2 | Filing of Documents with MCA, AOC-4, MGT-7 etc. for FY 2019-20 | Within 30 days/60 days of holding AGM | No relaxation so far | |

| 3 | Filing of Documents with MCA, for Companies which is pending to be filed (except Increase in the Authorized Capital ( SH –7), Charge related documents (CHG –1,4,8,9) |

As per Applicability with additional fees/ penalty/ prosecution |

Up to 30.9.2020 without additional fees No prosecution/penalty if filed till 30.9.20 |

Company Fresh Start Scheme of 2020 (Conditions to apply and certain cases are excluded) |

| 4 | Any document due to be filed till 31 st Aug2020 for an LLP |

As per Applicability with fine |

Up to 30.9.20 without additional fees No prosecution/penalty if filed till 30.9.20 |

LLP Settlement Scheme of 2020 |

| 5 | DIN KYC Verification | 30th April,20 | 30th September,20 | |

| 6 | Violations regarding CSR Reporting, Inadequacies in Board Report, Filing Defaults, delay in holding AGM etc. |

These were considered criminal in Nature and subject to prosecution of concerned Directors etc. |

These violations have now been decriminalized Withdrawal of 14000 prosecution cases Power of RD increased |

Majority of Compoundable offences to be shifted to Internal Adjudication Mechanism, |

| 7 | Penalties for Default by Small Companies, OPC, Producer Company and Startups |

As Applicable | Penalties Lowered | Provision of Part IX A(Producer Companies) of Companies Act 1956 introduced in Companies Act,2013 |

| 8 | MSME Return for half year ending 31 st Mar,20 |

30th April 2020 | 30.09.2020 | |

| 9 | Return of Deposit in DPT- 3 for FY 2019-20 |

30th June 2020 | 30.09.2020 | |

| 10 | Board Meetings-Gap between two meetings |

Not to exceed 120 days | increased to 180 days | Applicable till 30.09.2020. |

| 11 | Board Meetings – where accounts were being approved /Board Report |

Video conferencing not allowed |

Allowed till 30.6.2020 | No Relaxation where approval of Prospectus, amalgamation etc. & financial statement by Audit committee |

| 12 | Companies (Auditor’s Report) Order, 2020 |

Applicable from FY 2019- 20 |

Applicable from FY 2020-21 |

|

| 13 | Meeting of Independent Directors |

The independent directors are required to hold at least one meeting in a year, without the attendance of non-independent directors and members of management |

For the year 2019-20, if the Independent directors of a company to hold even one meeting, the same shall not be viewed as a violation |

|

| 14 | The requirement of filing a declaration for Commencement of Business by newly incorporated enterprises |

Within 6 months of incorporation |

Additional time of 6 months allowed |

|

| 15 | Minimum residency in India under Section 149 of Companies Act |

Minimum residency- period of at least 182 days by at least one Director of every company |

Non- compliance shall not be treated as violation |

|

| 16 | Requirement under section 73(2)(c) of CA-13 to create the deposit repayment reserve of 20% of deposits maturing during the financial year 2020-21 |

before 30th April 2020 | shall be allowed to be complied with till 30th June 2020. |

|

| 17 | The requirement to invest or deposit at least 15% of amount of debentures maturing in specified methods of investments or deposits |

before 30th April 2020, under rule 18 of the Companies (Share Capital & Debentures) Rules, 2014 |

may be complied with till 30th June 2020 |

|

| 18 | General Meetings of Members-EGM/AGM |

Video conferencing was not allowed |

Video Conferencing allowed until 30th June 2020 |

Detail procedure prescribed in MCA circulars |

| 19 | Compliance of Secretarial Standards |

SS-1 & SS-2 are compulsory in Nature |

Relaxation is given as per Guidance Note dt.15.4.2020 by ICSI |

|

| 20 | Minutes of the meetings Refer Secretarial Standard (SS-1 & SS-2) |

To be physically signed where minutes kept physically & with DSC when in Electronic form |

can be digitally signed by Chairman |

But after Lockdown needs to sign physically |

| 21 | The signing of documents by Directors Rule 8 of Companies (Registration Offices and Fees) Rules, 2014 for. Authentication of documents |

Physical Signing mandatory for Notices and Balance Sheet etc. |

No Relaxation However, may refer to The Information Technology Act 2000 and Evidence Act. |

MCA should come out with detail guidelines |

| 22 | Signing by Auditors /CA | Physical Signing mandatory ( Except where DSC allowed) |

signing through DSC allowed |

As per ICAI Announcement dated 13.04.2020 |

| 23 | UDIN by CA | Latest within 15 days from the date of signing the attestation document |

No Change |

5. Labour Laws & Other Acts

| S.No | Compliance | Original Status | After Relief Measures | Remarks |

| 1 | MSME Definition | Manufacture:- Micro if Investment if <25 Lacs, Small if investment <5cr and Medium if <10cr Services:- Micro if Investment <10 Lacs, Medium if investment <2cr and Medium if Investment <5cr |

Manufacture & Services, same criteria Micro—Investment less than 1 CR &Turnover less than 5CR Small—Investment less than 10 CR & Turnover less than 50CR Medium—Investment less than 20 CR &Turnover less than 100CR |

Registration certificate should be obtained for availing different benefits like concessional Loans, Payment within 45 days etc. -Emergency Credit Line to Businesses/MSMEs from Banks and NBFCs up to 20% of entire outstanding credit as on 29.2.2020 |

| 2 | Moratorium of Term loan and Deferment of Interest on Working Capital |

As per original Terms | moratorium extended till August 31, 2020 |

|

| 3 | Export Credits (Pre and Post Shipment Payment against Imports (under FEMA Regulations) |

9 months 6 months |

15 months 12 months |

|

| 4 | Application under Service Export from India Scheme (SEIS) for FY 2018-19 |

31.3.2020 |

31.12.2020 |

|

| 5 | For filing various reports etc by listed companies under SEBI Regulations |

As applicable |

Extended normally by one month |

|

| 6 | For companies employing up to 100 workers (for workers covered under PMGKY) |

Payment of 12% |

support is extended for |

|

| 7 | Contribution to PF for all establishments for next here months Except Central and State public Sector Undertakings |

12% for Employer and |

Reduced to 10% for both |

No penalty action due to delay in payment for period under Lockdown |

| 8 | Contribution to PF (Establishments up to 100 employees and 90 per cent of those earning less than Rs 15,000 per month) |

12% for Employer and |

Payment from March to |

Very few organization will be able to fulfil this criteria |

| 9 | Non Refundable Advance to workers from their PF Accounts |

Non-refundable |

PF Withdrawal of 75 per |

|

| 10 | Contribution to ESI |

The due date for filing ESI |

Due date of ESI |

No Penalty/prosecution for the delay in deposit of dues for the Lockdown period |

| 11 | Various Provisions of Labour Laws |

As per Existing |

Relief being provided |

Note:

(For Private Information only and not for quoting. Can be used for own consumption only after ascertaining the correctness of the information. Advised to consult your Tax Consultant/Adviser in case of any clarification or further guidance.)

Read the copy: