Section 112 of CGST Act: Appeals to Appellate Tribunal(Updated till July 2024)

Section 112 of CGST Act

Section 112 of CGST Act

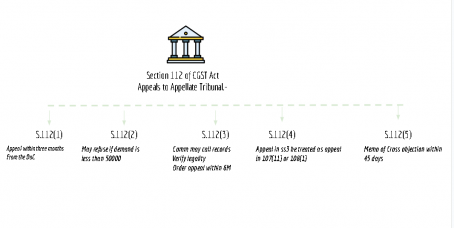

“(1) Any person aggrieved by an order passed against him under section 107 or section 108 of this Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act may appeal to the Appellate Tribunal against such order within three months from the date on which the order sought to be appealed against is communicated to the person preferring the appeal.

(2) The Appellate Tribunal may, in its discretion, refuse to admit any such appeal where the tax or input tax credit involved or the difference in tax or input tax credit involved or the amount of fine, fee or penalty determined by such order, does not exceed fifty thousand rupees.

(3) The Commissioner may, on his own motion, or upon request from the Commissioner of State tax or Commissioner of Union territory tax, call for and examine the record of any order passed by the Appellate Authority or the Revisional Authority under this Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act for the purpose of satisfying himself as to the legality or propriety of the said order and may, by order, direct any officer subordinate to him to apply to the Appellate Tribunal within six months from the date on which the said order has been passed for determination of such points arising out of the said order as may be specified by the Commissioner in his order.

(4) Where in pursuance of an order under sub-section (3) the authorised officer makes an application to the Appellate Tribunal, such application shall be dealt with by the Appellate Tribunal as if it were an appeal made against the order under sub-section (11) of section 107 or under sub-section (1) of section 108 and the provisions of this Act shall apply to such application, as they apply in relation to appeals filed under sub-section (1).

(5) On receipt of notice that an appeal has been preferred under this section, the party against whom the appeal has been preferred may, notwithstanding that he may not have appealed against such order or any part thereof, file, within forty-five days of the receipt of notice, a memorandum of cross-objections, verified in the prescribed manner, against any part of the order appealed against and such memorandum shall be disposed of by the

Appellate Tribunal, as if it were an appeal presented within the time specified in sub-section (1).

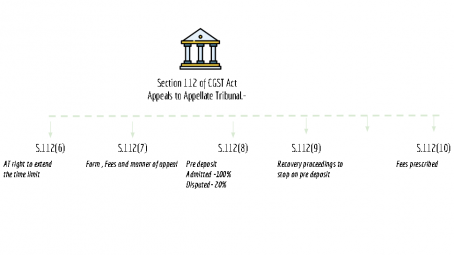

(6) The Appellate Tribunal may admit an appeal within three months after the expiry of the period referred to in sub-section (1), or permit the filing of a memorandum of cross-objections within forty-five days after the expiry of the period referred to in sub-section (5) if it is satisfied that there was sufficient cause for not presenting it within that period.

(7) An appeal to the Appellate Tribunal shall be in such form, verified in such manner and shall be accompanied by such fee, as may be prescribed.

(8) No appeal shall be filed under sub-section (1), unless the appellant has paid––

(a) in full, such part of the amount of tax, interest, fine, fee and penalty arising from the impugned order, as is admitted by him, and

(b) a sum equal to twenty per cent. of the remaining amount of tax in dispute, in addition to the amount paid under sub-section (6) of section 107, arising from the said order, in relation to which the appeal has been filed.

(9) Where the appellant has paid the amount as per sub-section (8), the recovery proceedings for the balance amount shall be deemed to be stayed till the disposal of the appeal.

(10) Every application made before the Appellate Tribunal,—

(a) in an appeal for rectification of error or for any other purpose; or

(b) for restoration of an appeal or an application, shall be accompanied by such fees as may be prescribed”

Related Topic:

Draft appeal to appellate authority

As given in CGST Act

Consultant