Expert Knowledge,

Straight from Practitioners.

Tax tips, legal guides, and financial advice written by the same verified CAs, Advocates, and Advisors you can consult on ConsultEase.

Whether Transfer of Development Rights is “Sale of Land”

Whether Transfer of Development Rights is “Sale of Land” Introduction As per Paragraph 5 of Schedule III ‘sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building’ shall be treated as neither supply of goods not the supply

Reversal of Input Tax related to Unsold Inventory on the Date of Completion Certificate or First Occupation

Reversal of Input Tax related to Unsold Inventory on the Date of Completion Certificate or First Occupation Article 366(26A). Meaning of Service [(26A) “Services” means anything other than goods; Inserted by the Constitution (One Hundred and First Amendment) Act, 2016, w.e.f. 16.9.2016 CGST Act, 2017-

Contractual Obligation To Pay To Vendors After 180 Days – A Controversy On ITC Reversal

Contractual Obligation To Pay To Vendors After 180 Days – A Controversy On ITC Reversal Management of cash flows during the COVID-19 pandemic presents novel challenges. To manage cash flows, Taxpayers would reshape their payment plans to vendors in this crucial time. The buyers of

GST -Goods and Services Tax , learn basics

GST implementation on July 1st, 2017: GST was implemented in India in 2017, 1st July. It is the biggest tax reform in India. GST subsumed a number of indirect taxes. Earlier our constitution allowed levy of tax either by center or state. 101st Constitution amendment

Issues in Taxation of Joint Development Agreement (JDA) Transactions – Under GST & Income Tax

Issues in Taxation of Joint Development Agreement (JDA) Transactions – Under GST & Income Tax In my last write up – Joint development agreement – Taxation under Income Tax & GST published in the month of April 2020 I have discussed taxation aspects of

The relevant date for computation of time limit for the refund to be calculated from the last date of last month of the quarter

The relevant date for computation of time limit for the refund to be calculated from the last date of last month of the quarter Karnataka High Court in Suretex Prophylactics India (P.) Ltd. [2020] 116 taxmann.com 566 (Karnataka) on 05-05-2020 Service Tax Refund of Cenvat

Legislative Competence of Rule 36(4) of CGST Rules 2017

Legislative Competence of Rule 36(4) of CGST Rules 2017 1. Rule 36(4) was inserted vide Notification No- 49/2019- Central Tax dated 09.10.2019 subsequently amended vide Notification No- 30/2020 Central Tax dated 03.04.2020 2. Condition for the availment of the Credit under Rule 36(4) of CGST

Blocked Credit Under Section 17(5)

Blocked Credit Under Section 17(5): The Orissa High Court 2019-TOIL01088, in the case of Safari Retreats (P) Ltd, which permitted availement of ITC on GST paid on raw materials such Cement, Steel, Sand, Construction Material, Sanitary, Electrical, Wooden items and other tax paid items for

CBIC Notifies Extension of Due-Dates For Payment Under SVLDRS

Notification No. 01/2020- Central Excise (N.T.) G.S.R (E)- In exercise of the powers conferred by sub-section (1) and (2) of Section 132 of the Finance (No. 2) Act, 2019 (23 of 2019), the Central Government hereby makes the following rules to amend the Sabka Vishwas

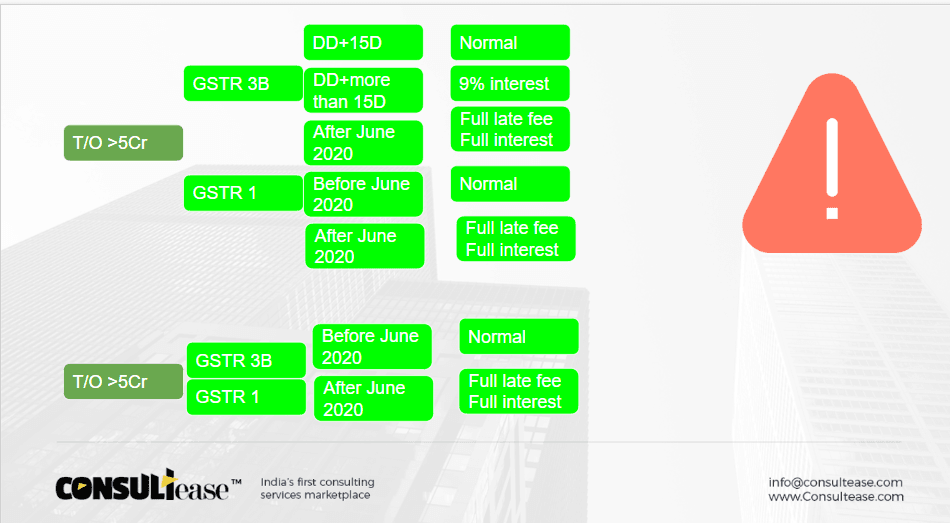

GST Compliance

GST ComplianceCaution: Not every compliance is deferred in GST

Caution: Read before you move, Not every compliance is deferred in GST Not every compliance is deferred in GST. Yes, Pls take care before generalizing the extension. Check the necessary compliances and guide your clients to follow them. Many notifications with relaxation. We need to go

CA Shafaly Girdharwal

CA Shafaly GirdharwalBar on refund of ITC not reflecting in 2A: Is it ultra vires ?

ITC not reflecting in 2A , No refund as per Circular 135/05/2020 Refunds in GST went through a lot of amendments. Kept playing with the online and offline stuff. Many of the issues were settled. Circular No.135/05/2020 – GST tried to sum up the things.

CA Shafaly GirdharwalUpdated Provisions of Input Tax Credit under GST

Input Tax Credit under GST The input tax credit has been defined as per Act in our previous article. It means the credit of Input Taxes paid on inputs, capital goods, and input services. The Input tax in relation to a registered person, means the