Expert Knowledge,

Straight from Practitioners.

Tax tips, legal guides, and financial advice written by the same verified CAs, Advocates, and Advisors you can consult on ConsultEase.

Notification No. 41/2020 – Central Tax

Notification No. 41/2020 – Central Tax [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 41/2020 – Central Tax New Delhi,

Notification No. 39/2020 – Central Tax

Notification No. 39/2020 – Central Tax [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 39/2020 – Central Tax New Delhi,

GST Compliance

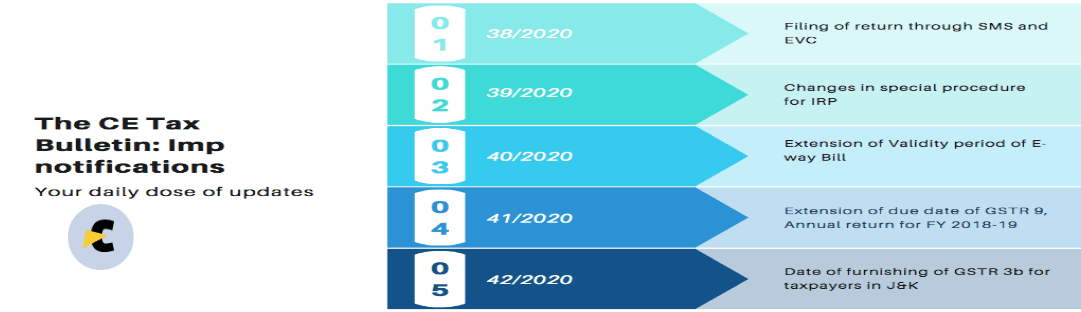

GST Compliance5 New Notifications in GST: Annual return date, E-way bill validity and more

5 New Notifications in GST 5 New Notifications in GST yesterday. These notifications are issued via the Gazette of India. They are not yet at the CBIC website. But they are quite important. Let us have a look at their summary. Filing of the return

101st Constitution Amendment Act

Sec 1: Short title and commencement. (1) This Act may be called the Constitution (One Hundred and First Amendment) Act, 2016. (2) It shall come into force on such date as the Central Government may, by notification in the Official Gazette, appoint, and different dates

GST Compliance

GST ComplianceTaxability of Joint Development Agreement

Taxability of Joint Development Agreement Joint Development Arrangement (JDA) has always been a bone of contention between the assessee and the tax department. The dispute lies is in measuring the correct amount of tax both under Direct and Indirect Taxes. Hence it has always been

SEARCH, SEIZURE AND RELEASE OF SEIZED GOODS

SEARCH, SEIZURE, AND RELEASE OF SEIZED GOODS CONSTITUTIONAL VALIDITY OF SEARCH AND SEIZURE A search by itself is not a restriction on the right to hold and enjoy the property. No doubt a seizure and carrying away is a restriction of the possession and enjoyment

Renting/ Leasing/ Licensing/ Transfer of Right to Use of Goods, Immovable Property and Intellectual Property Rights

Renting/ Leasing/ Licensing/ Transfer of Right to Use of Goods, Immovable Property and Intellectual Property Rights Renting/ Licensing/ Transferring the Right to use can be classified under four categories 1. Immovable Property a. Residential Property for Residential Use- SAC 9972 b. Residential Property for Commercial

Updated provisions of Place of Supply under GST

Provision on Place of Supply under GST Determination of Place of Supply What is the place of supply in GST? GST is a destination-based tax, i.e., the goods/services will be taxed at the place where they are consumed and not at the origin of supply.

Updated provisions of Registration under GST

Registration under GST [Section 22 to Section 30 of CGST Act and Rules 8 to 26 of CGST Rules along with FORM GST REG 01 to GST REG 30] Registration of any business entity under the GST Law implies obtaining a unique number known as

Updated provisions of Valuation under GST

Valuation under GST SECTION 15: VALUE OF TAXABLE SUPPLY[RULE 27 TO RULE 35] As GST is payable as a percentage of the value of supply, it is thereby important to determine the value of taxable supply as per the GST Law. Section 15 of the

Updated provisions of Time of Supply under GST

Time of Supply under GST After ascertaining whether a transaction falls under the definition of supply, we come to the next pertinent issue, the date of the charging event i.e. the date when the liability of the tax arises which is covered by the provisions

Updated provisions of Supply under GST

Supply under GST The determination of the taxable event is one of the most important matters in every tax law. It is that event which on its occurrence creates or attracts the liability to tax. The taxable event under GST shall be the supply of goods